Bringing people together - a year in M&A

A look at 2014's record acquisition activity

"It's not about the money. It's about my sanity." Such were the closing words of Markus "Notch" Persson on his personal blog post confirming the sale of Mojang to Microsoft and his leaving the company. It's probably a little trite, but not exactly unfair, to point out that $2.5 billion buys a lot of sanity. As we saw last week, it also buys a lot of house.

Microsoft's purchase of Mojang - which, let's be honest, was actually a purchase of Minecraft - would have been a headline in any year, but in 2014 it was the focal point of a trend which saw M&A activity in the industry soar. Five deals worth a billion or more dollars each dominated that landscape: Mojang, Oculus, Twitch, Giant and FunPlus, totalling $6.1 billion.

You'd be forgiven for thinking that fish of this magnitude might indicate otherwise empty waters, but even without the big five, the value for mergers and acquisitions up to and including Q3 2014 was running equal to that of 2013 entire, already a record year. Include the headline acquisitions and you have a total of $12.5 billion, double that of 2013.

"The biggest deals of the year to Q3 2014 show how indies can become unicorns, and that smaller companies are creating magic that major corporates will buy"

Tim Merel, Digi-Capital

Looking at the economics of these mega-deals, it's clear that some were fairly traditional, whilst others make less immediate sense. Digi-Capital's Tim Merel offered us these interpretations.

"The biggest deals of the year to Q3 2014 show how indies can become unicorns (e.g. Mojang), and that smaller companies are creating magic (e.g. Oculus) that major corporates (e.g. Microsoft, Amazon, Facebook) will buy:

- 1. Microsoft/Mojang ($2.5B at 8x revenue and 20x profit): a long term strategic investment to nurture the Minecraft community for Microsoft's future cloud, mobile, virtual reality and wearables platforms.

- 2. Facebook/Oculus ($2B at reported 87x revenue): a long term strategic investment in the potential of virtual reality as a growth platform.

- 3. Giant Interactive take private ($1.6B at 8x revenue and 12x operating profit): Giant's Chairman and financial backers take advantage of the current phase in the investment cycle, betting Giant is more valuable as a private company.

- 4. Amazon/Twitch ($970M at reported double digit revenue multiple): Amazon accelerates both its video and games initiatives, while also scoring a competitive win.

- 5. Zhongji/FunPlus games assets ($960M): Chinese industrial conglomerate buys its way into the future, providing the remaining FunPlus team with financial firepower to reinvest in mobile.

Oculus is a particularly stark gamble, here, then. Whilst it's unlikely that games will be the main focus of Facebook's use of the tech, it's remarkable that such a vast price would be paid for an idea which remains unproven in the commercial realm, with a consumer release still some way off. The Oculus deal might be something of an anomoly,

Some other notable players spent 2014 hoovering up new businesses, too. Unity, which seems almost unstoppable in its drive to ubiquity, picked up Applifier, Tsugi and Playnomics, before sparking acquisition rumours of its own. After its purchase by Facebook, Oculus picked up Nimble VR and 13th Lab, whilst Autodesk acquired Bitsquid and Shotgun Software.

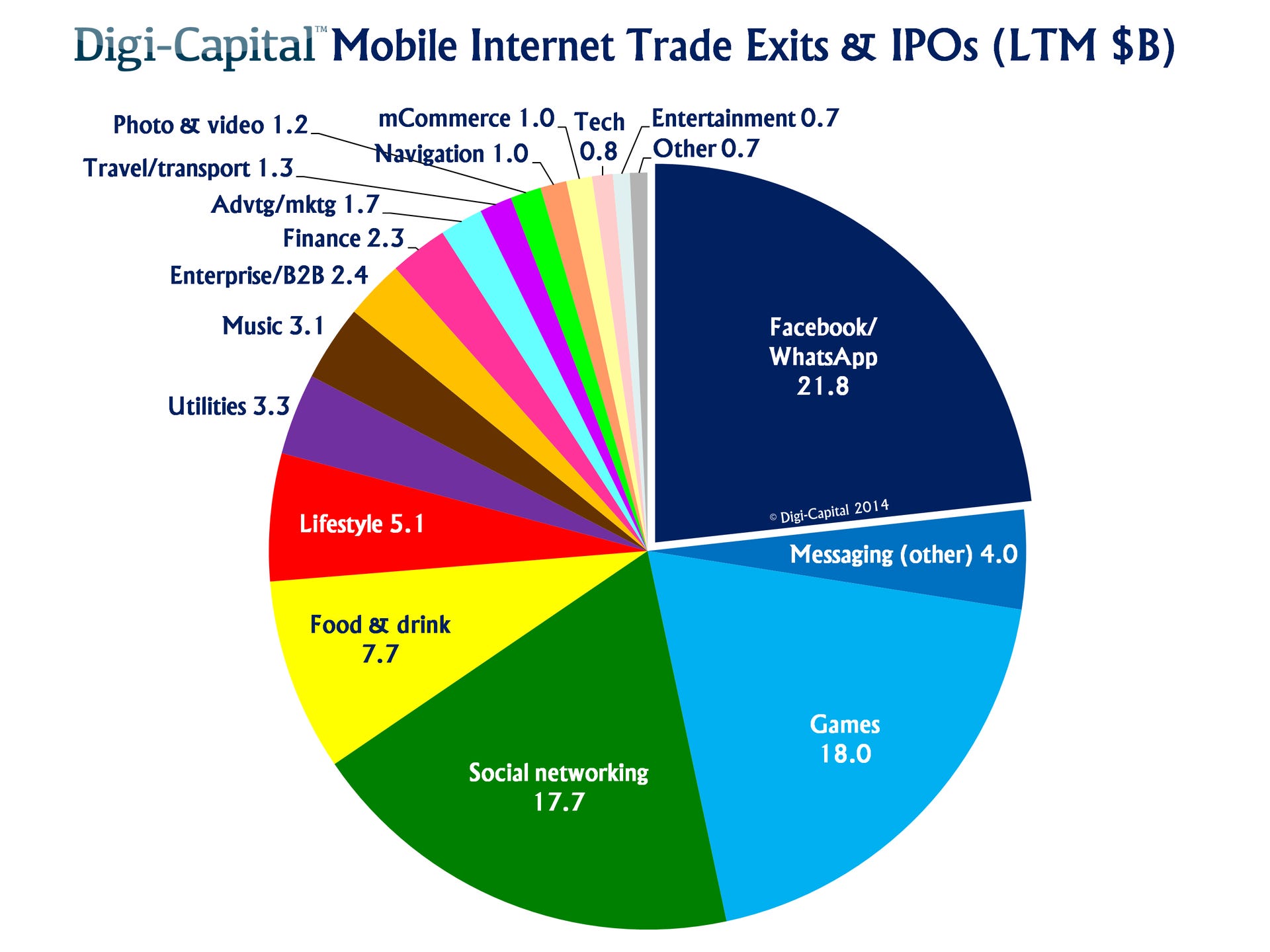

Mobile remains a huge focus for M&A activity accounting for $4.6 billion of the year's spend, a figure which jumps up sharply with the inclusion of IPO money.

"The big driver for the games industry is mobile, and we don't see that changing any time soon," says Merel. "Looking at the total exit market for mobile internet more broadly (both trade exits/M&A and IPOs), mobile games were the second largest driver at $18B of exits in the 12 months to Q3 2014. This is second only to messaging (with the $21.8B Facebook/WhatsApp deal), which makes that performance even more remarkable."

This is partially a reflection of companies buying their way into inflated markets, but there's also an element of protectionism, as evinced by last year's Zynga buyout of Natural Motion. That, says Merel is just one of the big companies "stopping mobile insurgents from eating their lunch." Others have been simple territory buy-ins, giving established giants new footholds in hard-to-reach markets like China, or Asian operators the familiarity and accompanying credence afforded by western brands.

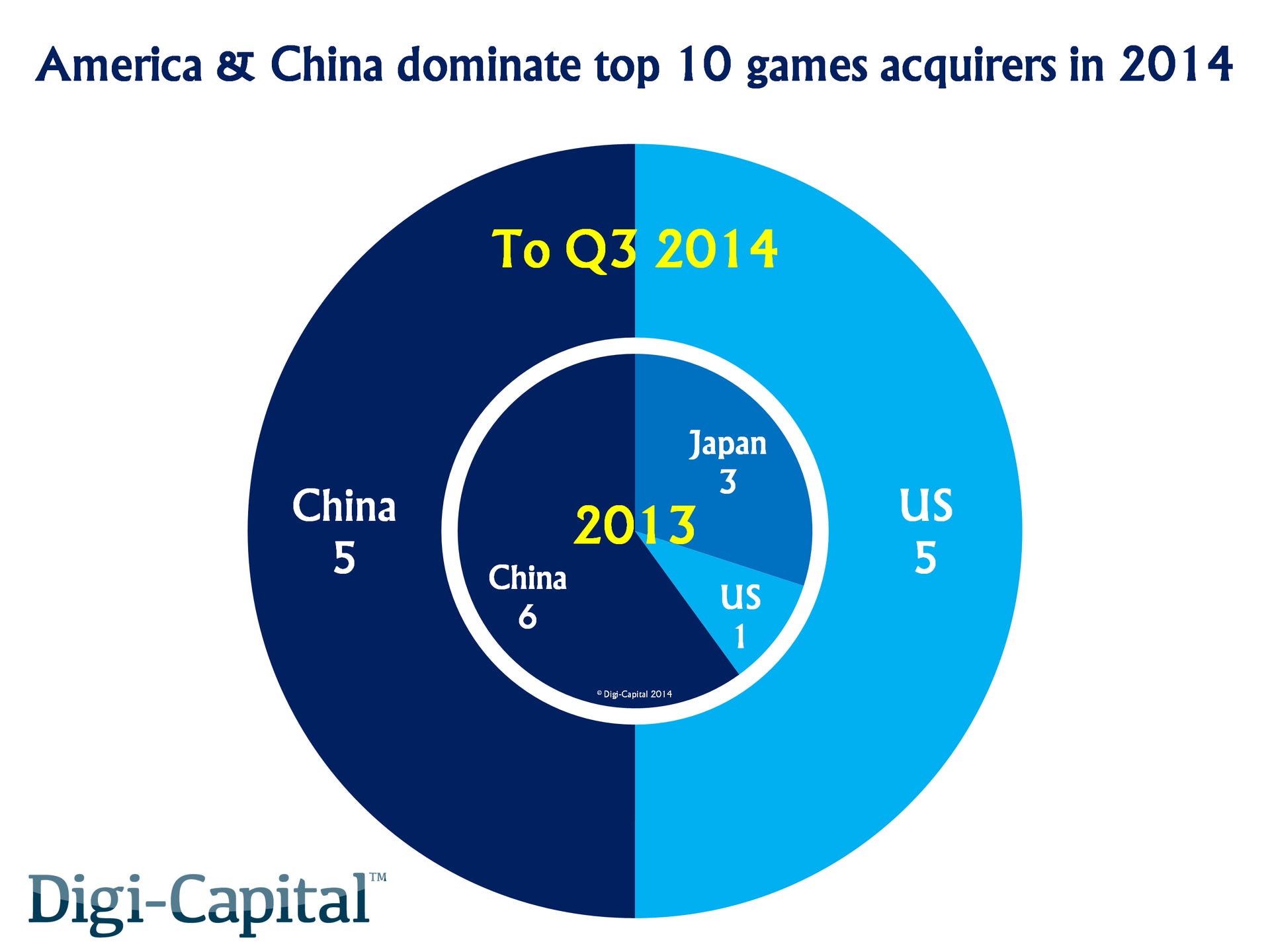

In fact, 2014 was a year in which the west reasserted itself in the M&A market, with 50 per cent of the big buys coming from US companies and the rest from Japan and China. Just one year previously, that ratio stood at 90 per cent in Asia's favour.

"The companies being bought come from all over the world," says Merel. "So entrepreneurs and investors wanting a good exit need relationships across America and Asia. Europe has been more of a sellers' than a buyers' market in recent years."

2014 is going to be a tough year to match, but who looks like a tempting target for next year? Primarily, if the rumours have any semblance of truth to them, Unity has to be a target. The company's stellar growth, whip-smart strategy and tremendous reach amongst the up and coming generation of developers would make them a very smart buy in the $1-2 billion range, but company CTO Joachim Ante has strenuously denied the possibility. With Ricitiello now on board, could Unity be looking at an IPO instead?

Elsewhere, Codemaster owner Reliance has been making a lot of noises about expanding its mobile gaming portfolio, with chief executive Manish Agarwal telling Reuters, "we will go full steam in the January and February time frame in terms of identifying studios. Gaming is going to be the largest share of the pie of entertainment time spent, and Reliance would like to be a sizeable player in that space." Many of those targets are expected to be European or North American.

Facebook is unlikely to be finished with its Oculus-related buys, too, although again these will likely be tech rather than directly game-focused. Expect Microsoft to bring at least one indie under its wings, whilst Sony retains its slightly more hands-off approach.