Video game sales evade strong economic headwinds (for the time being)

Sparkers consultant Sam Naji looks back at game sales in 2022, including how new releases helped weather catalogue declines

As we begin 2023, the economic headwinds against the UK are very strong, currently facing a triple whammy of economic pressures.

According to the Consumer Prices Index (CPI), inflation rose by 11% in the 12 months to November 2022. UK taxes are some of the highest on record; new analysis by the Tax Payers Alliance has found the five year average tax burden is at a 70-year high. And consumers are not feeling very confident, with PWC reporting that consumer confidence stands at -44 – a sentiment worse than the -26 at the start of the pandemic.

With news like that, every household has had to make hard choices during this cost-of-living crisis. One area of the household budget that could be construed as an "easy decision" is the amount spent on entertainment. When it comes to food, house payments and energy, discretionary spending on entertainment, by contrast, is often way down on the list of priorities.

Therefore, you would be forgiven in thinking spending on video games will take a huge hit. Interestingly, on a macro level, this has not yet happened. If anything, spending on some video game titles are breaking records.

In the last several weeks the headlines from Gameindustry.biz have been astonishing with record beating sales. Headlines included Pokémon Scarlet and Violet becoming the fastest selling games in Nintendo history, Splatoon 3 sales surpassing 3 million units in Japan after its first two months, God of War Ragnarök having the biggest launch in its franchise history, and Call of Duty Modern Warfare II launch sales doubling that of Vanguard.

These headlines of record-breaking sales would be impressive by themselves, but when combined with news that numerous video game publishers are also making record revenues, the industry is currently riding a wave that flies in the face of the dispiriting economic prognostications.

The trend in sales growth this year has not been confined to the fourth quarter of 2022. Throughout last year, new games sales rocketed past those compared to the new games released in 2021.

New releases

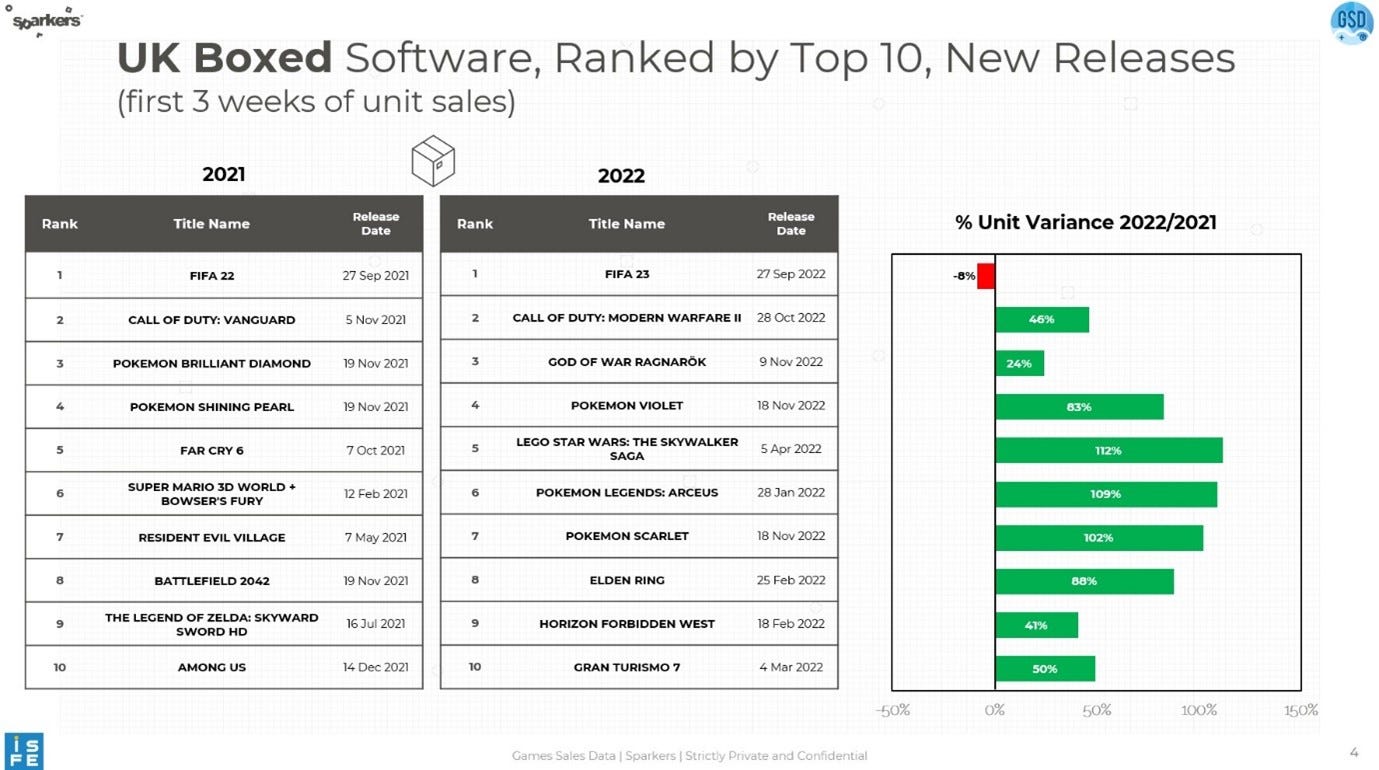

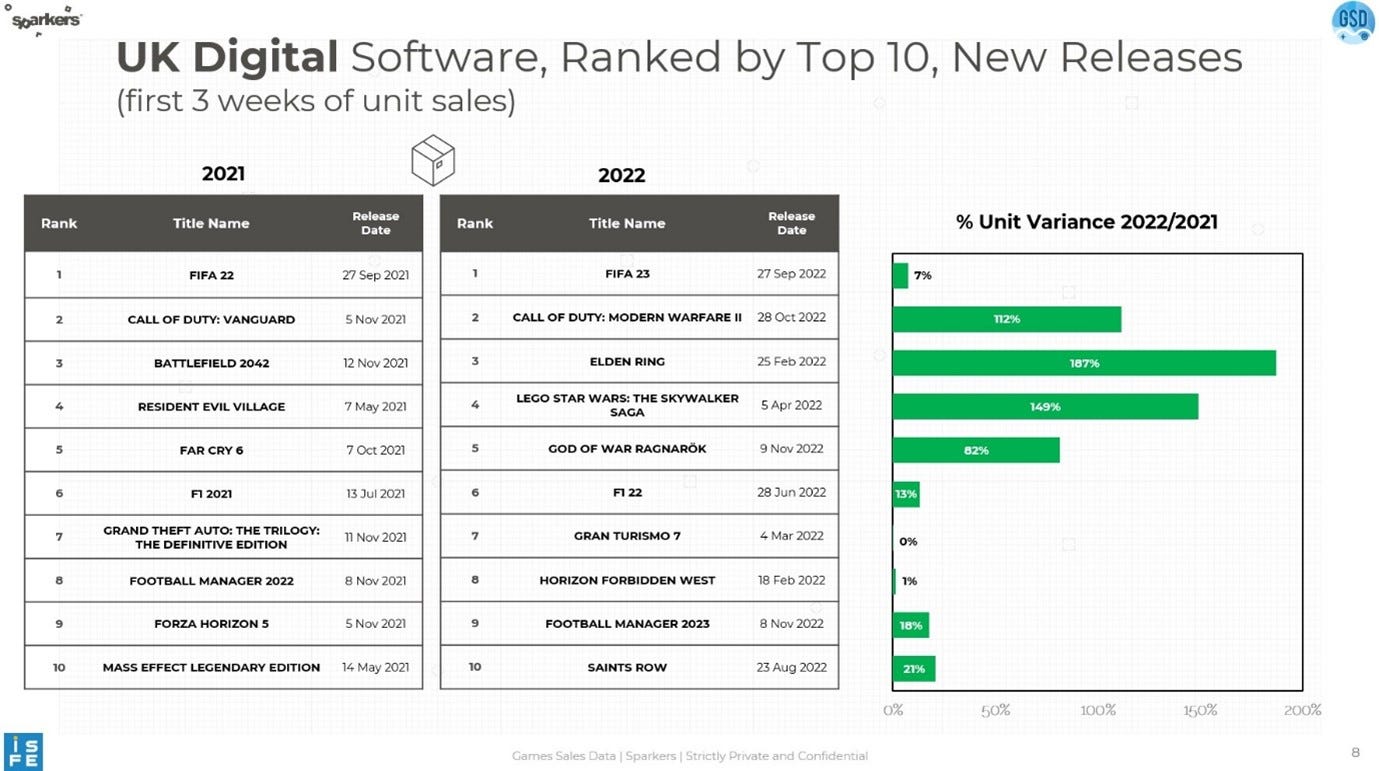

The two tables below show the UK ranked top 10 new games released within their first three-week launch window. The first several weeks in market are often the most profitable time in sales for most new releases. Table 1 shows the sales from boxed physical disc full games. Table 2 shows the sales from GSD-tracked full game digital downloads (see chart at the bottom of this article for the list of participating publishers).

The top 10 new boxed games generated 31% more sales in 2022 than their 2021 counterparts.

Like the growth in retail disc sales, unit sales for full game digital downloads increased by 52% in 2022 compared to 2021.

When you combine new game releases for boxed sales and digital (full game) downloads, there where an additional 1.5 million units sold in 2022 compared to 2021.

Legacy letdown

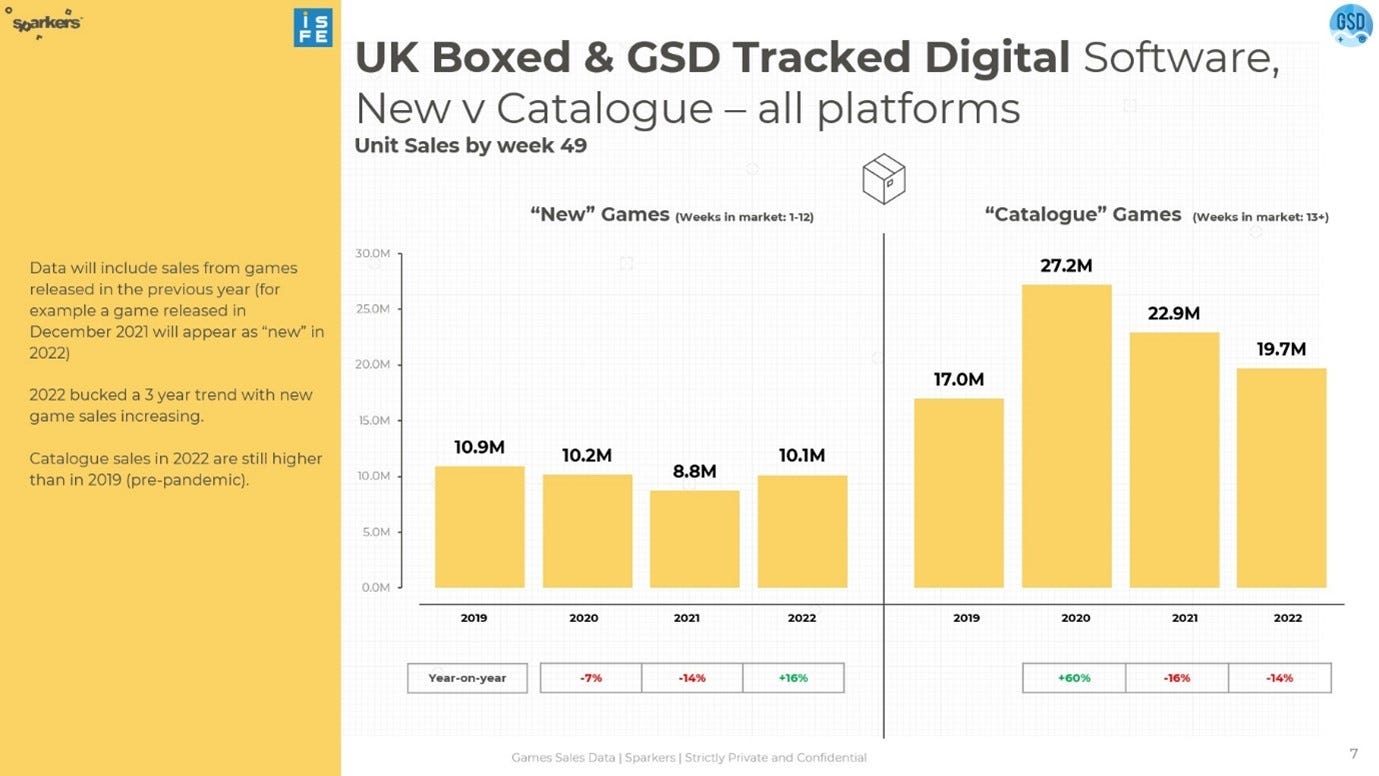

One of the criticisms levelled at 2022 was the lack of new releases after April. As opposed to a general lack of appetite to buy games, evident in Table 1 and 2, it was the lack of new releases during the spring and summer periods that had many speculating 2022 was a bad year for game sales overall. This assumption was somewhat borne out when looking at total sales, year to date. By week 49 cumulative unit sales for boxed games were lower by 10% in 2022 compared to 2021. For full-game digital downloads, unit sales had declined by 2%.

To a large extent, this industry lives and breathes on new content, and that can directly impact spending further down the line

What is evident from Chart 1 (below) is that a significant share of the decrease in sales came from "catalogue" games, namely those games which have been in market for over 12 weeks. A significant proportion of the downturn in catalogue sales for 2022 was due to the fact the COVID-19 pandemic surged sales in 2020 and 2021. In the first 49 weeks of 2020, catalogue sales increased by more than two-thirds compared to the same time the year before.

Tellingly, as the pandemic hit the release slate of new games between 2020 and 2021, the knock-on effect was to see an overall decline in sales for "new" (the first 12 weeks of sales of releases) games year-on-year.

It was only by this year, in 2022, that the decline in sales for new games reversed. Unit sales for new games in 2022 increased by 16% compared to 2021, almost reaching 2019 levels.

The paradox in 2022 is that as fewer games released, the appetite to buy new increased. Consumers are speaking with their wallets. They are in the market to purchase more new games and less catalogue. We just need more releases! Luckily it looks like a lot of the postponed releases will come out in 2023.

Black Friday

Just as the signs on which direction video games sales are going is mixed, so too are the signs mixed if the game industry can weather a downturn in the economy. If one were to look at the Black Friday week sales alone, the story feels downbeat. The combined unit sales for full-games physical boxed games and digital downloads declined 3% during 2022 compared to 2021.

Just as the COVID-19 pandemic spurred on a wave of video game spending, a recession could do the same

One must however consider other factors which can confound the simple statement that "the games market is experiencing a downturn." For example, the decline in Black Friday sales this year could be somewhat attributed to that quiet period in the spring and summer months when few games released. Catalogue sales can only satisfy consumer appetites so far. Once you bought and own a catalogue game, you do not need to re-purchase.

As the demand for catalogue games increased during the time of the pandemic lockdowns, it disrupted the normal market for games. The whole market will experience a downturn if no new games come on the market to replace the catalogue games bought. Unless new product comes along to fuel catalogue, sales for older games will decline as time goes by. To a large extent, this industry lives and breathes on new content (whether that be full games or DLC), and that can directly impact the scale of spending further down in time.

For publishers, and to a large extent for gamers, the decline in full game sales is not the complete picture. Many new games today offer huge value for money. Today, some games come with hundreds of hours of gameplay or offer live service experiences that can last for a very long time. For many gamers these types of games have somewhat replaced historic single-player narrative games, which could have been completed within ten hours or so.

To compound matters, most "casual" gamers will only play one or two new games in a year, preferring to stick to their favoured titles or franchises. The certainties that once built the video game market in the past have shifted as new ways to play games have come onto the market. FIFA is now supported by FIFA Ultimate Team transactions, GTA 5 is supported by GTA Online, and Call of Duty is supported by Warzone. This all implies greater engagement in retaining client base. For example, publishers today are just as keen to know about Daily Active Users (DAUs) for their current games as they are for sales for their new releases. For a publisher or developer, the chances are a new game's release is the beginning of the story, not the end.

The state of streaming

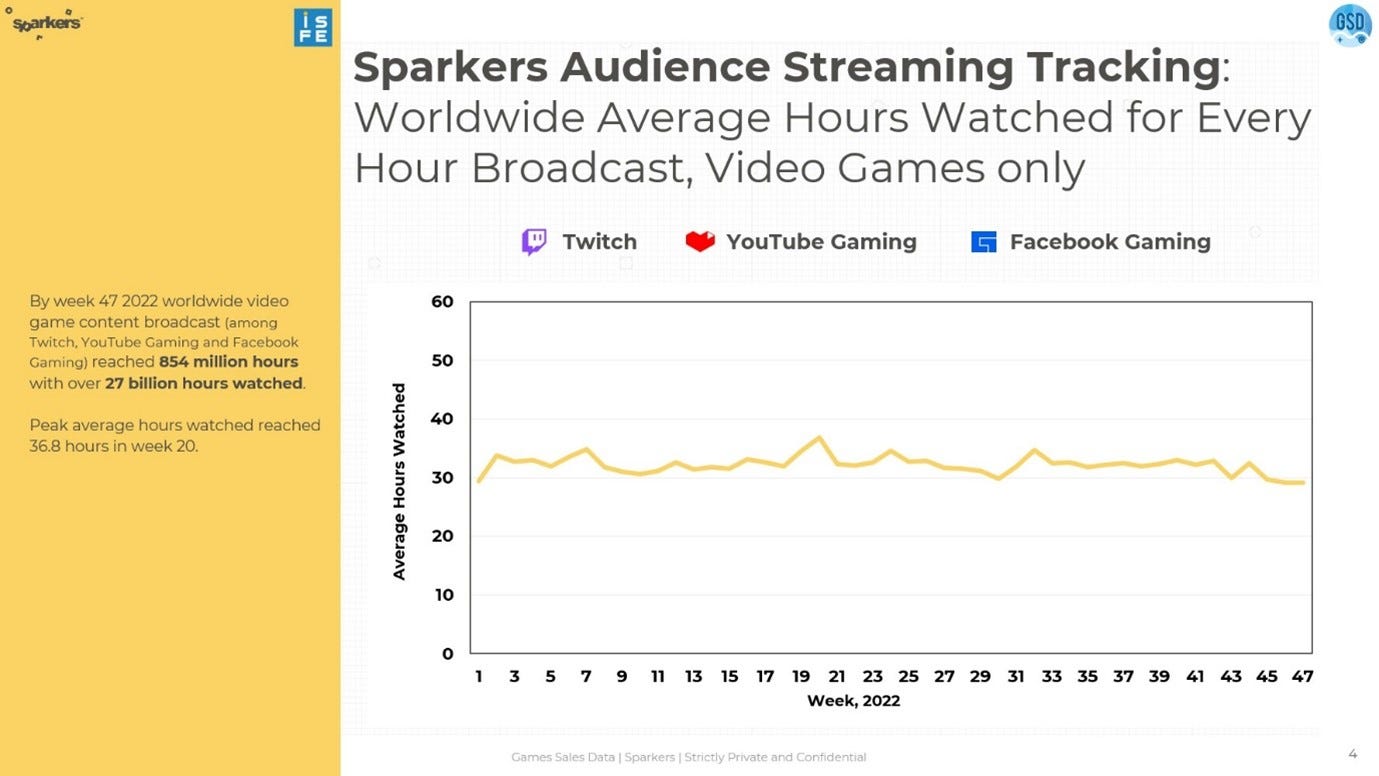

One way to analyse how the market has shifted is to look at video streaming. Throughout 2022, gamer engagement on streaming has not declined. Chart 2 illustrates this trend.

The premier Belgium video game market research company, Sparkers, has a streaming tracking tool called Audiences, which monitors streaming on Twitch, YouTube, and Facebook Gaming with acute granularity. Audiences showed a worldwide weekly average watch between 30 hours to 35 hours for every hour broadcast. This was the weekly average watch for games and/or gameplay only.

The fact the average watch did not waver below 30 hours during 2022 is cogent that interest in gaming is just as strong at the start of the year as it is as at the end. One way to look at this is to imply that interest in gaming is not directly correlated by the economic pressures of rising costs or household economic anxiety.

For example, Netflix recently increased its subscriber base by 2.4 million members during its Q3 2022 financial disclosure. This was when households faced increasing costs and strained entertainment budgets. By the same logic one could also expect growth in video game spending, albeit a modest growth.

Households must still make entertainment spending decisions and if that means spending more time at home or in front of a screen, this should favour TV subscriptions and video game spending. Just as the COVID-19 pandemic spurred on a wave of video game spending, a recession could, inadvertently, do the same. This increase may not take the form of full game spending, but it could see an increase in microtransactions or subscriptions such as Game Pass and PlayStation Plus. We will get a better idea of the situation when the calendar Q4 financials of video game publishers and developers are released.

Recession proof?

Historically, the video game industry has been somewhat resilient when the economy is in a bear market (i.e. a market in which share prices are falling). This is because the video game business follows its own business cycle somewhat. The decline of video game sales usually comes from video gamer apathy in existing console systems. Increases in video game spending usually come from the releases of new consoles and technological advances, less so with the state of the consumer purse.

Increases in spending usually come from new consoles and technological advances, less than the state of the consumer purse

One only needs to look at the financial statements of some AAA publishers to realise they have never made so much money today in their lifetime. To be at maximum revenue during so much economic uncertainty is some achievement. A lot of the credit goes to how video games have evolved with new technologies. Consumer panel after consumer panel indicate that more and more people classify themselves as "gamers". This is probably the most important factor on ascertaining the health of this industry. A video game market can continue to expand even if the core gamer spends less, offset by more spending by a growing pool of casual gamers.

Although fewer games have been released lately there is no doubt competition in the market is still very strong. The amount of spending on games, whether it be on PC, console or mobile, does not look as if it will go into reverse gear any time soon.

Both publishers, and gamers, have come to terms that the video game market has shifted in the last decade. Publishers have diversified revenue streams and gamers look to maximise value for money. The good news is that the video game market is catering for all audiences, whether rich or poor, whether core or casual, whether single player narrative or multiplayer, whether AAA or indie.

So far this means that the video game market is successfully evading the economic headwinds, for the time being anyway. As to whether this will continue by 2024 is unknowable, but I will leave you with this final thought. Times are tough, both domestically and internationally, and this is when escapism and imagination will play a pivotal role in the mental wellbeing for many.

We all need to have fun, now more so than ever, and this will bold well for video games.

ISFE's Games Sales Data provides the most comprehensive UK panel for physical software and tracks digital full-game sales directly from publisher sales.

Sparkers is a Belgium company that operates the panel Games Sales Data (GSD) for ISFE. Audience is a new streaming tracking service provided by Sparkers which combines real time data on streaming services with sell-through data for both the physical market and digital markets.

If you are interested to know more about Sparkers, GSD and Audiences and how they can help you with video game analytics please contact info@sparkers.com.