GameStop's meme stock rallies don't fix its decline | Opinion

GameStop's stock market drama masks the fact that the realities of being a physical retailer in a digital market haven't changed

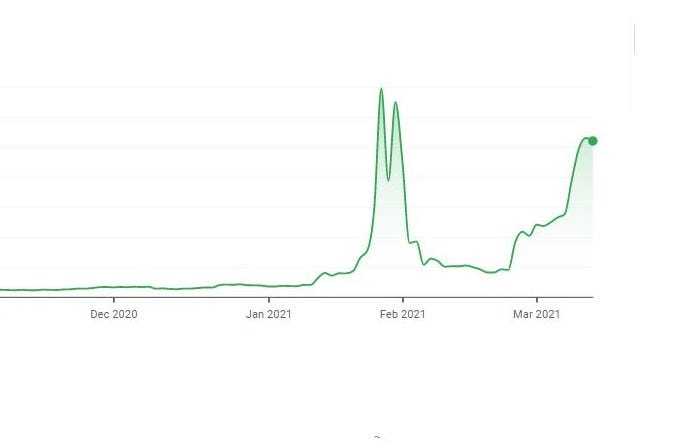

For anyone who has kept up with the games business over the past decade or two, there's something utterly surreal about seeing GameStop's name in the biggest headlines of the financial press for weeks on end.

The story of the once-dominant retailer's slow decline in the face of the relentless growth of digital distribution ought by rights to have been one with a pretty familiar and predictable final act. Instead, it's the focus of one of the most unusual and unpredictable stock market dramas in years, and the company's stock ticker -- GME -- has become almost totemic for an extremely online group of retail investors who believe, perhaps with some justification, that they've found a way to play the market in their favour.

The specifics of what happened to turn GME into a "meme stock," beloved of Reddit's now notorious WallStreetBets (WSB) forum, are complex and as far as the games industry is concerned, not actually terribly important. Prior to this recent media attention WSB was best known for eye-watering "loss porn" posts, in which people would share screenshots of the huge financial losses they'd incurred with stupid, high-risk investments. Its interest in GME was sparked by claims that the retailer had been targeted by hedge funds who seemed to believe that the firm was going bankrupt soon, leading them to take enormous "short" positions to benefit from its demise -- and thus leaving themselves enormously exposed to risk (due to being on the hook to pay out potentially huge sums to buy in order to cover their short positions) should the firm not only survive, but actually see a rally in its share price.

GameStop's long-term decline is undeniable, but a great many companies hold on for a long time

As crazy as everything happening around the stock has been, the underlying observation that GameStop isn't actually on the brink of bankruptcy is a perfectly reasonable one. GameStop's long-term decline is undeniable, but a great many companies plateau after such a decline and hold on for a pretty long time, if not indefinitely; GameStop, which has pretty decent assets and generally manages to eke out some profit from all of its stores, always seemed pretty likely to belong to that category, rather than being the kind of firm that would dramatically implode in the end.

The idea that GameStop's death-knell was being sounded very prematurely isn't unique to the Reddit meme mob; investors like Michael Burry (of The Big Short fame) took positions in the company over the past few years on the basis of similar logic. (Full disclosure: I don't usually buy shares in games-related companies, but following a high-risk personal investment strategy of buying shares in companies recommended by anyone who's been played by Christian Bale in a movie, I bought some shares around the same time. It's been a fun few weeks.)

Whichever way things go -- whether GME share prices crater back down into the single digits or soar to the moon, as the meme stock evangelists hope and believe -- the current furore will eventually die down. What will remain is GameStop's actual business. For all that its executives are undoubtedly enjoying seeing its valuation soar into the tens of billions, that doesn't actually mean an enormous amount to the underlying company, whose ability to convert any of that share price success into financial succour is extremely limited by restrictions on its capacity to issue new shares. So once the hype dies down, what will actually remain?

It's 2021; deciding that you want to be the Amazon for gaming right now is about 15 years too late

GameStop's strategy for now appears to be to capitalise on the current publicity it is enjoying by focusing attention on its efforts to pivot the business. This week it announced a new committee that will focus on finding ways to build out digital aspects of GameStop's business. Featuring activist investor and Chewy founder Ryan Cohen in a lead role, the committee's plans are described in ambitious terms such as making the company into "Amazon for gaming."

The problem with this big, flashy announcement is that in many ways it simply underlines -- several times, and in blazing red ink -- just how unsuccessful GameStop's attempts to pivot to digital thus far have been. It's 2021; deciding that you want to be the Amazon for gaming right now is about 15 years too late, not least because there's already an Amazon for gaming -- it's called Amazon. The point where GameStop might have effectively leveraged itself into a powerful position in the online retail and digital distribution spaces is long behind us.

Bear in mind that there was probably a point when GameStop could quite comfortably have bought the nascent Amazon -- or perhaps more relevantly, a company like Valve, whose burgeoning Steam platform it ought to have seen as an opportunity rather than an irritant. Now, literally decades behind the curve, it's going to take some seriously innovative and lateral thinking to figure out exactly what the GameStop brand is worth and how it can be turned into something more meaningful than a slowly declining chain of stores in America's slowly declining malls.

It's not just the company's previous efforts at digital and online pivots that have been failures. A great many of the things that are often suggested as viable paths forward for the company -- such as focusing on merchandise and more broadly "gamer-related" goods, rather than just on selling physical games -- are actually things it has been trying to do for some time, with very limited success. The concept of being a "destination" for gamers rather than just a retail storefront isn't a bad one; it's just that the company hasn't actually figured out how to make that happen, and it turns out that filling shelves with T-shirts and those weirdly overpriced bobblehead toys doesn't seem to be the secret sauce for either footfall or per-store revenue.

There are other things it could try. GameStop has dabbled in being an esports venue, which could be one avenue forward if it's done right. In stores with enough space the concept of a VR arcade franchise might work -- but being realistic, all of the remaining options to stimulate new growth are pretty high risk strategies at best.

Being realistic, all of the remaining options to stimulate new growth are pretty high risk strategies at best

The problem to some extent is that GameStop's scale -- which is enormous, with the company still operating thousands of stores even after its downsizing -- owes itself to the one thing that it cannot possibly recreate or return to. The company became a behemoth purely and entirely due to its lock on the market for second-hand games, which it was able to buy cheaply (often offering only store credit) and sell on at a major mark-up, often close to full-price. The same copy of a game could pass through GameStop repeatedly, with the retailer taking a generous cut of each cycle. This occurred at a scale which not only drove GameStop to an absolutely dominant position in retail, but which actually distorted the overall market for games for many years.

The enthusiasm with which the rest of the industry embraced major online retailers and digital distribution is, in no small part, actually down to GameStop itself. As a dominant retailer, it was far from a benevolent dictator; not many people who had to deal with GameStop during the era when it could make or break a game's launch have anything positive to say about the experience. When digital distribution began to make inroads, all the while slowly tolling a funeral bell for the second-hand business, a lot of publishers and developers couldn't embrace it quickly enough. When firms like Amazon and Walmart, which have little or no interest in the second-hand market, began to dominate physical sales, many companies were more than happy to see it.

It's vanishingly unlikely that GameStop will find -- whether through its digital pivot or its ideas about being a gamer destination -- another business model that's quite as profitable as the second-hand market was for such a long time. Even success in its current state would be measured more in terms of successfully managed decline than in any meteoric return to growth. It's also worth noting that as long as GameStop continues to operate so many stores, its fortunes are tied up to some extent with those of America's malls in general.

These woes are not unique; they are a microcosm of a broader malaise for that kind of retail, which has been exacerbated by the pandemic but only in a way that accelerated an underlying trend towards low footfall, empty units and declining relevance. Whatever solution GameStop finds as it continues -- with more and more urgency -- to try and reinvent itself is going to have to be one that works in the context of those broader problems.

The meme stock rollercoaster has brought attention and focus to GameStop for a while, and may, at least, afford the company some minor options in terms of raising capital to fund its turnaround plans. But the stark reality of how tough its turnaround will be hasn't changed a bit. No matter how much Reddit likes the stock, the real challenge is finding a way to make consumers like the stores once more.