eSports: The missed billion-dollar opportunity for publishers and platforms

The Chernin Group's Ed Chang sees huge potential in eSports publishers fully embracing the third-party ecosystem

eSports is no longer a secret. Every week there's a new report detailing how big the industry can really be, but there's also an elephant in the room. Startups and third parties are finding it hard to identify their segment of the space and monetise, due to a complex relationship with the companies who create the actual games - the publishers.

Lay of the land

The traditional sports ecosystem is dominated by three models of organisation. The most decentralised sports, like the PGA Tour or NASCAR, consist of largely independently organised competitions, which are sanctioned and governed by an administrative body and are open to any qualifying athlete. From there, we have typical leagues like the NBA or Premiership, which have a set number of recurring teams and players, and are extensively managed by a league front office that's owned by each team.

eSports are quite different. If you choose to race without NASCAR or play basketball without the NBA, there's nothing - and no official body - that can prevent you from replicating the experience. No one 'owns' racing or basketball, but someone does own Overwatch, and if you want to play you essentially have to go through that company. If you wanted to create your own eSports league, your ability to market or represent it would be entirely dependent on the legal team of the game's publisher. Furthermore, the core experience is fully controlled by that publisher.

"No one 'owns' racing or basketball, but someone does own Overwatch, and if you want to play you essentially have to go through that company"

Leagues that are operated or endorsed by publishers can do unique things - e.g. item drops, exclusive/first-release capabilities, bundled original content - and offer unique monetisation opportunities. Three months before The International, the annual world championship for Dota 2, Valve sells interactive in-game items that directly contribute to the tournament prize pool. This model has been so successful that, in 2016, the prize pool reached $19.17 million.

Most tier-one publishers also handicap the data streams that the public can leverage. Whereas in traditional sports there are multiple providers of a firehose of sports data, game publishers offer barebones APIs that allow access to little more than character information and select match data. Valve offers an open API but, as events this year have demonstrated, it can shut off access and change policy at any time. On the platform side, Twitch is miles ahead of its competitors in terms of creating an external ecosystem thanks to its two year head-start and passionate developer community, but it maintains an ever more precarious balance between build vs. buy.

Because of these walled gardens, the investible opportunities within eSports often end up being features not products, which set them and their investors up for more of an acquihire than a Twitch-esque exit. There's a strong argument to be made to publishers that working with third-party developers will lead to a stronger overall bottom line, foster innovation and provide defensibility.

Economics 201

It's no secret that being a top publisher is a lucrative business. Activision reported $1.57 billion in revenue for Q2 of 2016 and EA $1.271 billion. It's rumoured that Valve's 2015 revenues reached $3.5 billion in 2015, and Riot Games' over $1.6 billion. It's not hard to see why partnerships with third parties and external API infrastructure aren't a priority with so much money flowing, but that's shortsighted. As publishers start thinking about how to monetise beyond game licenses and IAP, every moment not spent developing the ecosystem is a wasted one.

This isn't unparalleled, and we can see examples of where large platforms in other verticals have made the decision to invest in their future, often early on in their company lifecycle. Salesforce, an enterprise software company, has a market cap of $50 billion. A report last year by IDC put the opportunity front and center: the AppExchange currently generates 2.8x the revenue of Salesforce itself and is expected to grow to 3.7x the size of Salesforce.

"As publishers start thinking about how to monetise beyond game licenses and IAP, every moment not spent developing the ecosystem is a wasted one"

Slack, the enterprise collaboration tool darling, also gets it. Even before raising money in April 2016, at a $3.8 billion valuation and boasting over 1.25 million paying users, they announced the Slack fund in December 2015 - an $80 million investment into supporting new integrations. Slack and Salesforce could have gone the closed route and developed these integrations and products internally, but they understood that the immediate revenue trade-off was well worth the ability to focus on creating the best core product possible, in addition to leveraging minimal company resources.

Now to everyone's favourite eSports comparison : traditional sports. During the height of the daily fantasy sports craze in 2014/15, the NBA entered a multi-year partnership with FanDuel that gave it an ownership stake. The NFL expanded its partnership with Providence Equity in 2013, investing $300 million to participate in, "media and technology deals where it believes the league could help play a strategic role." And these are just a few examples. Partnering with and investing in new properties allows older, larger establishments to participate in the upside of nascent industries quickly and cheaply.

Publishers are thinking about the shelf-life of games. The NFL and NBA will both be around in 25 years, but what about League of Legends or Counter-Strike? Opening up the ecosystem not only benefits players and fans by allowing them an outlet to interact with their favorite IPs, but ultimately enhances the core value of those IPs and gives publishers an opportunity for additional exposure through revenue share, API fees and strategic investments.

Defensibility and innovation

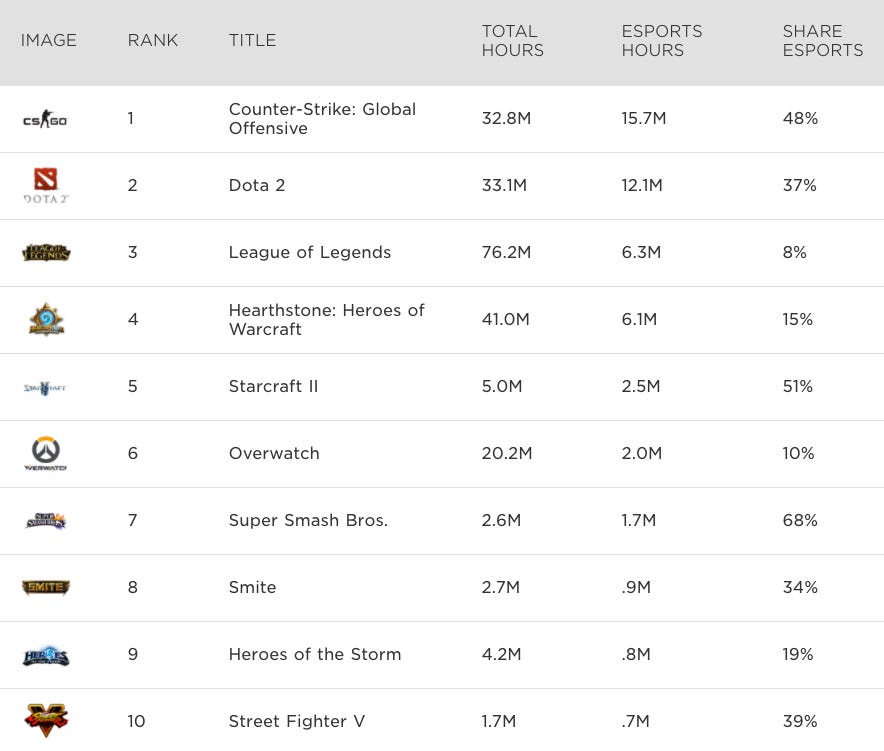

In addition to commercial benefits, let's look at network effects. Valve is the publisher of both Counter-Strike: Global Offensive (25 million+ copies sold, 8.2 million+ players in the last two weeks), and Dota 2 (87 million+ times downloaded, 11 million+ active players in the last two weeks.) While the titles have richer histories than virtually any other competitive esport, Valve's open API, developer tools and hands-off approach has contributed to their sustained success and status as two of the top eSports titles.

1: Valve developer tools / Steam API: Valve has created a set of developer tools and an API that allows for custom creation of maps and in-game items, as well as access to match data and transaction facilitation. As a result, Workshop currently has 125k+ approved items for CS:GO and 50k+ for Dota 2. Valve's developer tools have also been the foundation of sustainable, revenue generating businesses that keep players loyal, like:

- FaceIt ($15mm Series A): 10mm+ game sessions/month

- ESEA (acquired by ESL): industry leader in professional CS:GO leagues and anti-cheat technology

- Kickback (YC W15): 8mm+ "money matches" played, 50,000+ players

"Publishers are thinking about the shelf-life of games. The NFL and NBA will both be around in 25 years, but what about League of Legends or Counter-Strike?"

For Valve, the boost in user acquisition, overall engagement and free marketing is well worth the short-term revenue trade-off.

2: Competitive ecosystem: Valve has taken a hybrid approach to competitive eSports, where it has a handful of officially sanctioned major tournaments sandwiched between multiple leagues and LAN events. This has led to a very robust landscape, with events and leagues like the ESL Pro League, ELeague, FaceIt Esports Championship Series and Gfinity, ESL One and IEM. These streams of revenue have contributed to a high demand for professional CS:GO players, leading to lucrative contracts and opportunities.

3: The most lucrative has been the in-game skins economy, which allows players to purchase crates that contain different cosmetic versions of CS:GO weapons or Dota 2 items. During major tournaments, Valve has offered exclusive stickers that generate up to high six-figures for qualified teams. Valve has also allowed free reign on opening up use cases within this skins economy, which led to wagering, gambling and marketplaces (Bloomberg estimated yearly transaction volume to be >$7 billion.) Variations of this model have since been followed very conservatively by multiple franchises, including Call of Duty, Halo, H1Z1 and Overwatch.

On the platform side, Twitch's dominance in livestreaming can largely be credited to going all-in on eSports first, but Twitch also has numerous native or platform exclusive features for its users. Diving deeper, this experience is powered by a blend of features that were built in-house or created by third parties. Examples include:

- Bits, preceded by Streamlabs and StreamTip: direct donations from viewers are one of the foundations of a streamer's income.

- Clips, preceded by Oddshot, Plays.tv and Forge: allows viewers and creators to efficiently capture highlights and share to different social media channels.

- Subscriptions / Partner Program and 3rd-party services (Revlo, Gamewisp and Curse/Discord integrations): subscriptions are another big source of income for streamers, and the third-party services all add further value to a sub and reduce churn.

- TwitchPlays: what started out as a fun social experiment (TwitchPlaysPokemon) is now its own category to interact with potential customers for publishers.

- Chatbots (Moobot, Nightbot and Xanbot): automated assistants that help moderate chat to prevent spamming and inappropriate behaviour.

Facebook Live has launched to much fanfare, and given the massive distribution channel it will always be a huge threat. However, until it can get to feature parity Facebook Live will need to rely on traditional media partnerships or viral hits to create consistent content. These types of partnerships don't scale when we're talking about the individual streamers and professional players that have played a large part in getting Twitch to 100m+ MAUs, although the signing of G2 and Heroes of the Dorm is a good first step. YouTube Gaming is farther along and is doing a great job of starting to launch some analogous features.

How, then, should publishers look to partner with entrepreneurs and third parties? I'd like to see publishers create a vehicle, individually or collectively, in the model of Disney Accelerator, to offer mentorship, funding and support to kick-start the next generation of eSports businesses. Publishers should be developing their games as platforms, not individual entities - tons of data are being generated and archived and there is a treasure trove of use cases for them.

I'm confident that we're slowly moving in the right direction. One day we'll see a truly open ecosystem with publishers and third parties living in harmony.

Ed Chang is an entrepreneur in residence at The Chernin Group (TCG), a privately held, independent media holding company founded by Peter Chernin, based in Los Angeles. TCG has built, managed, operated, and invested in businesses in the media, entertainment, and technology sectors around the world since 2010. You can find him on Twitter @ed_chang.