ConsolidationVille: Social Games M&A in 2012

Digi-Capital on social, mobile and middleware acquisition opportunities in 2012

Digi-Capital has just published its Global Games Investment Review 2012, and the free Executive Summary is available here. The complete 102 page review and individual sector reviews (mobile/tablet, social/casual, MMO, console, middleware and advertising) are available here.

Online/mobile games are forecast to grow the total video games software market in the 2015 financial year to $82 billion and take 50 per cent revenue share at $41 billion (14% CAGR 11F-15F). The acceleration in games investment and M&A also looks set to continue, driven both by underlying growth and fragmentation. However we see the big story as Social Games 1.0 M&A in 2012 - exit or consolidate (or you might miss the boat).

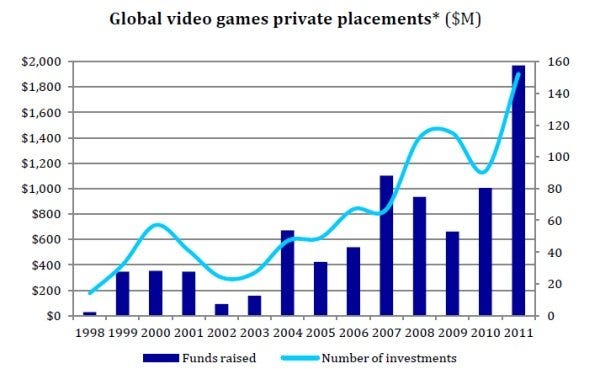

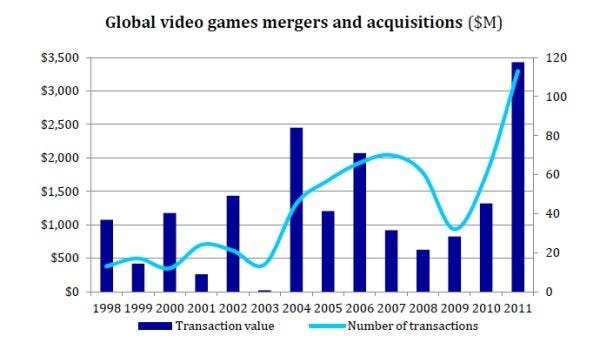

Games investment and M&A more than doubled in 2011

Games private placements grew value by 96 per cent to $2 billion, volume by 67 per cent to 152 transactions, and average fundraising round size by 17 per cent to $13 million. Together with Zynga ($1bn+) and Nexon ($1.2bn) IPOs, games investment value nearly quadrupled in 2011. Games M&A grew value by 160 per cent to $3.4bn, volume by 88 per cent to 113 transactions, and average transaction size by 38 per cent to $30.4 million.

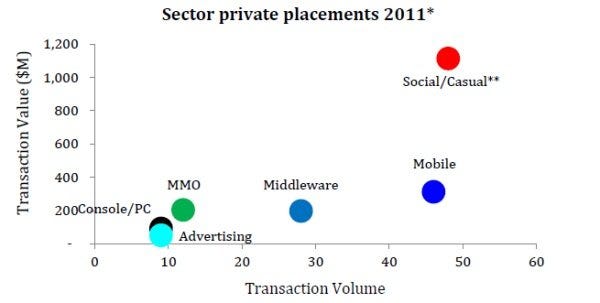

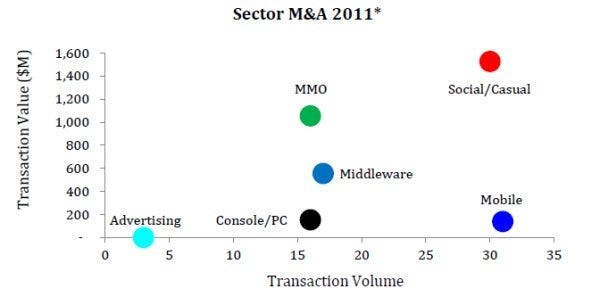

From a sector perspective, games private placement and M&A activity in 2011 were led by social, mobile, MMO and middleware.

Social Games 1.0 M&A in 2012 - exit or consolidate (or you might miss the boat)

Social/casual games dominated investment and M&A in 2011 (57 per cent of private placement value, 45 per cent of M&A value). The Zynga IPO may be the high water mark for Social Games 1.0, as it becomes harder to keep social games social (i.e. user acquisition and retention). Our detailed analysis of total games portfolio DAU (Daily Active Users) and average individual game DAU (see in the Social/Casual Games section of the full Review) shows some (e.g. Wooga, King), but not all competitors delivering in a crowded market. Current sector dynamics and the dealflow we're seeing indicates 2012 could be the year for Social Games 1.0 consolidating M&A.

Social-mobile and cross-platform are the next battlegrounds for games investment and M&A

Mobile/tablet games were second in transaction volume (30 per cent private placement, 27 per cent M&A) but not value (16 per cent private placement, 4 per cent M&A) in 2011 as this is an early stage market. DeNA (2011 >$1.4bn revenue at 50 per cent operating margin) and Gree (12 months to December 2011 >$1.4bn revenue at 46 per cent operating margin) show what investment in social-mobile games can deliver. Not surprisingly, we see mobile/tablet, social-mobile and cross-platform (iOS/Android/social network) games companies attracting serious interest from both investors and acquirers this year.

Free-to-play and new market entrants reinvigorating MMO M&A and investment opportunitiesMMO games were second (31 per cent) in M&A value due to large scale transactions, but only fourth (8 per cent) in private placement value in 2011 due to investment risk profile. Nexon (>$1.1B revenue at 58 per cent EBITDA margin in 2011) shows why the MMO market is moving towards free-to-play. We see consolidating M&A and investment opportunities through 2012 due to continued MMO market transition and growth.

Asian consolidating M&A and investment hold great promise, but local knowledge and relationship gaps remain

The strong Chinese, Japanese and South Korean games companies we work with are actively looking for Western M&A and investments, but local knowledge and relationship gaps remain. Similarly the western games companies we work with are looking for strong Chinese, Japanese and South Korean partners, but face the opposite side of the same challenge. By bridging relationships and different business/investment cultures, we see this becoming one of the dominant axes for games M&A and investment.

Console giants must accelerate pivot to online/mobile

Electronic Arts has led the way with blockbuster M&A of PopCap and Playfish, yielding synergies with The Sims Social. We think that the other cash generative console/MMO publishers still have a window of opportunity for online/mobile investments and M&A, before it becomes too late to change.

Middleware is the dark horse generating significant investment and M&A

Games Middleware was third by value in both private placements (18 per cent) and M&A (16 per cent) in 2011, despite being lower profile than consumer games sectors. High profile M&A from non-traditional sources such as Visa's acquisition of PlaySpan for $190 million shows the potential for middleware investors/management. We think that accelerating M&A and investment in online/mobile middleware should continue to be driven by growth in underlying online/mobile games markets.

So 2012 is shaping up to be a pretty interesting year for games investment and M&A.

Digi-Capital as a digital investment bank focused on games across America, Europe and Asia (China, Japan, South Korea).