Stock Ticker: Sony, Nintendo, EA show their strength

How have the world's stock markets responded after financial season?

The past few weeks have seen a host of financial announcements from game publishers and platform holders - some good, some bad, many indifferent. This makes it a good time to take a look at how those companies are performing on the stock exchanges and try to glean some insight into how the markets view their future potential.

It's probably worth starting with a familiar caveat - stock markets are not magic and their investors are rarely privy to any grand insight about the companies in question. Their actions, and hence the movement of stock prices, are not based on hidden knowledge, but on sentiment about a company's future performance. Stock markets often do silly things to share prices based on unfounded enthusiasm or excessive pessimism - but nonetheless, these prices are important, because their maintenance is often considered to be the main job of a public company's management team and their movements influence the income not only of senior executives but of many ordinary development and publishing staff. In short, these figures aren't mystical oracles of great truth, but they impact on the lives and incomes of lots of people in our industry; they're worth watching and understanding.

With that out of the way, let's take a look at our first set of companies - the platform holders.

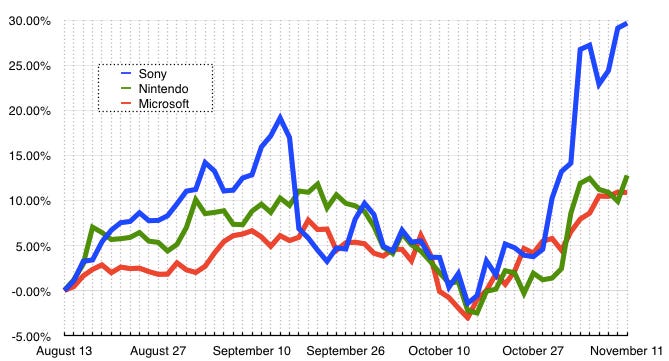

This graph, like all of those in the article, covers a three-month span, dating back to mid-August. The immediate thing that leaps out is the performance of Sony, which has performed well throughout the period but leapt ahead since mid-October. Microsoft and Nintendo, meanwhile, are both doing fine in this graph, but dwarfed by Sony's figures. Incidentally, get used to that massive dip around the first week of October; a scare on the financial markets drove almost every share price in the world down around that point, so we'll see it on most of the graphs in the article but it's not terribly relevant to the games sector specifically.

A graph like this is actually less informative than we might like - it pits an American company, Microsoft, against a Japanese company, Sony, without taking into account the underlying conditions in their national economies. In fact, year to date both Sony and Microsoft's share prices have performed similarly - they're both up about 30 percent on where they were at the start of January - but again, this is an unfair measure as they are based in countries whose economies are faring very differently from one another. In order to allow for this discrepancy, the easiest thing to do is to introduce another line to the graphs, an index representing the overall gains or losses of each stock exchange. For Japan we use the Nikkei 225, which aggregates the performance of 225 of Japan's largest companies; for America we use the NASDAQ 100, a smaller index but one more explicitly focused on the high-tech sector.

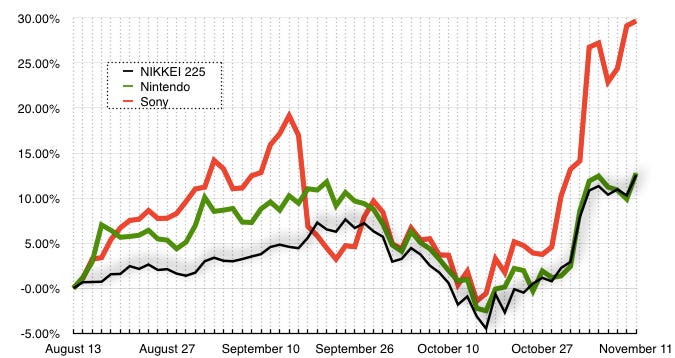

Here's how the platform holders stack up if we do exactly that and contrast them against the performance of their home markets. First up, the Japanese pair.

This graph suddenly makes Nintendo's performance look rather less impressive; it's essentially just been tracking the strong rise in the Nikkei stock market. Sony, however, has more than doubled the performance of the Nikkei since the market bottomed out in early October. We know the PS4 is doing well, despite the struggles of some of Sony's other divisions, but surely it doesn't account for this kind of performance?

Well, no, it doesn't; not entirely at least. Sony has had a pretty strong 2014 overall off the back of ongoing good sentiment about Kaz Hirai's leadership of the company and PS4's performance in particular, but the huge rise we've seen in the past month is based on different factors. See that rapid rise in the Nikkei around the start of November, which is mirrored in Nintendo's figures? That's the result of a major new round of quantitative easing (creating more money, essentially) by the Bank of Japan, which has driven the value of the Yen down to levels unseen since the 2008 financial crisis. A weaker currency (and renewed hope for a healthy inflation rate) is good for most Japanese stocks but especially for companies which export their wares, since they can now either drop their prices overseas to be more competitive, or retain their existing prices and make more profit. It stands to reason that Sony would be seen as benefitting from this more than Nintendo. Sony has been a stronger performer overseas than Nintendo; the 3DS and Wii U are by far at their strongest in the Japanese market, whereas the PS4's biggest markets are in Europe and the USA, and Sony also has many other lines for export.

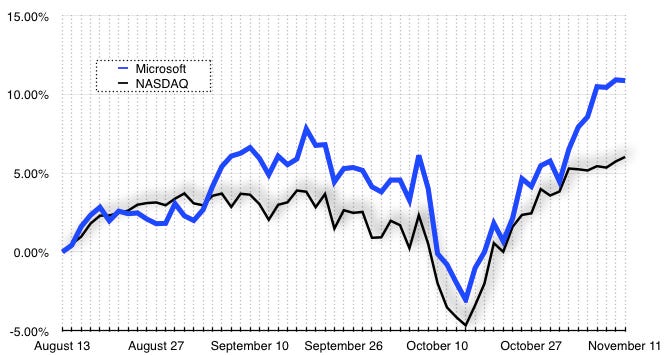

We can put Microsoft's figures into a similar context against the NASDAQ graph.

It's clear that Microsoft is doing well - better than the NASDAQ index, for the most part - but it's not spectacular. Indeed, the company's share price has had a good year overall and, like Sony's, is up around 30 percent for the year, but it's been a more gradual and perhaps sustainable rise than Sony's price. From a gaming perspective, though, that's unlikely to have very much to do with Xbox One. This is new CEO Satya Nadella's first year at the company and its share performance is more connected to his stewardship of the firm's lucrative enterprise and office software divisions, as well as its focus on cloud services. Consumer hardware such as the Xbox or mobile phones don't really figure in this picture overall - which is just as well, as neither side has put in the kind of performance that would thrill investors.

Turning now to third-party publishers, let's look first at the graph for the US' publicly listed publishers.

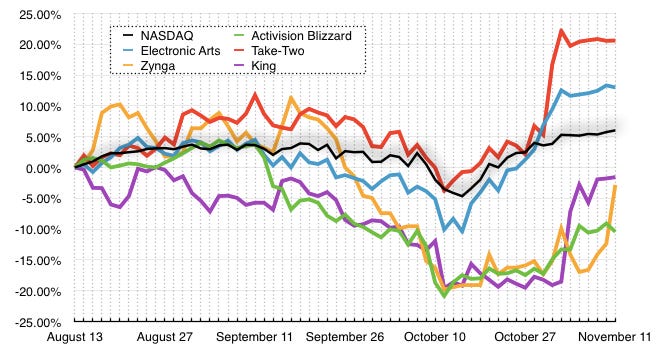

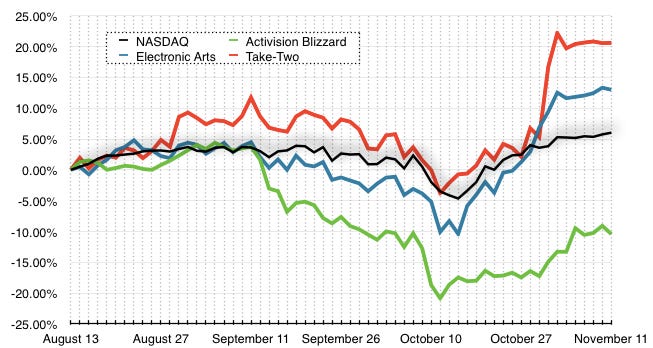

This is something of a mess, although we can clearly see that only two companies - Take-Two and EA - are on the right side of the NASDAQ's black line in the middle of this graph. It hasn't been a great three months for game stocks overall, then; perhaps we should take a closer look. The next two graphs divide publishers into two basic groups - the traditional publishers in the first group, and the newer mobile/social publishers in the second.

Looking at the three major publicly-listed traditional publishers in the USA, we can see that both Take-Two and EA have done really well, while Activision tanked much harder than the rest of the market in October and has recovered much more slowly. The big rises for EA and Take-Two in the past month are easy to understand; both companies reported results that were ahead of the market consensus, with EA being particularly lauded for the huge revenues it's earning from its digital titles. Both companies were upgraded by a number of influential analysts, which means a lot of investors bought into the stocks and drove the prices higher. Take-Two's stock moved further percentage-wise, but it's worth noting that EA's market valuation is more than five times Take-Two's, so it takes a lot more investment activity to move the needle for EA.

Didn't Activision also have a pretty stellar set of results recently, though? And hasn't Activision just had a couple of really huge launches in a row? First Destiny, then CoD Advanced Warfare, with Warlords of Draenor just around the corner? How come the markets haven't responded positively to that?

Again, it's worth remembering that markets respond to sentiment about future prospects, not facts about present performance (except where those facts help to predict future prospects). Investors in Activision already expected huge launches for Destiny and Call of Duty; in market parlance, those expectations were already "baked in" to the share price. Activision's poor performance in the past few months is based not on those launches being poor (which they were not), but on investors being uncertain about what the company is doing next. Destiny's mediocre critical response may have fuelled concerns about the game's much-vaunted potential as a 10-year franchise; the expected continuing decline in CoD's sales may be making investors nervous about Activision's ability to create a replacement franchise on the same scale. The company's firmly PC/console focused activity, lacking EA's prowess in mobile and social, is also a long-term concern. This being the stock market, there could also have been any number of daft rumours going around to undermine the price; but ultimately, the investors aren't sure about Activision's future. It's worth noting, though, that the company's valuation is still higher than EA's ($14.8bn to $12.9bn), so it's not like the firm is seriously hurting on the stock market right now - but it has been a tough couple of months.

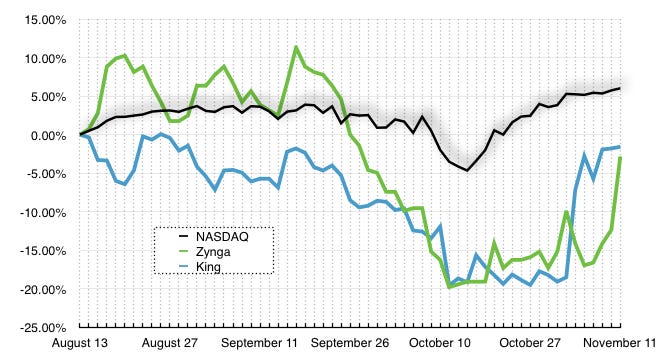

How about those newcomers in the mobile/social space? Given EA's performance was at least partially off the back of good mobile/social results, how did the companies devoted to that space manage?

Ehh... Not so great, actually. Mobile and social may be booming, but you wouldn't know it to look at publicly listed companies in this space. Neither Zynga nor King has covered themselves in market glory this year; they're both down about 25 percent for the full year (or in King's case, since its IPO back in the first quarter of the year). That trend continued in the most recent three months, with both firms slumping far harder than the rest of the market when things hit the skids in October, and taking much longer to recover. Zynga claims to be on the mend but still desperately needs to prove that it can evolve into a sustainable company; it's making more of its money from mobile now, which is a positive move, but it's still a long way from being a success story. King, meanwhile, is still "the Candy Crush company", and has yet to demonstrate that it's capable of replicating that success in a meaningful way. Until it does, it's unlikely to see much share price growth.

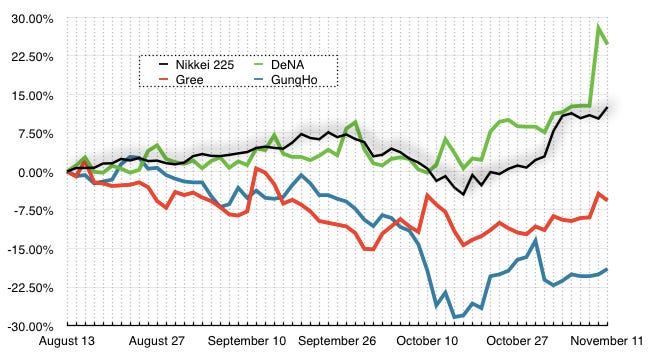

Let's cross the Pacific now and take a look at the other index with plenty of game-related stocks on it, the Tokyo Stock Exchange.

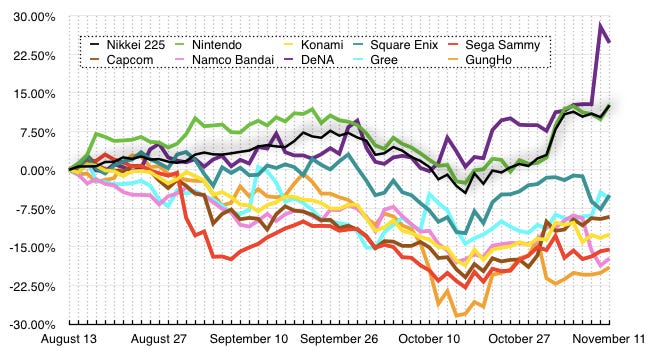

Tokyo has a lot of game-related stocks, so this graph is, frankly, a mess. There are only two things you can easily read from this - firstly, that DeNA has had a really good few weeks recently (better than expected quarterly results explain that last-minute spike), and secondly, that every other third-party publisher in the country has under-performed the Nikkei index in the past three months. The green line closely hugging the Nikkei index (in black, as ever) is Nintendo, so in spite of its well-publicised recent troubles, the Kyoto-based platform holder has actually been doing better on the markets than any other major game company, DeNA aside.

Let's repeat what we did with the US companies and break these into two graphs - one for traditional publishers and one for mobile/social firms.

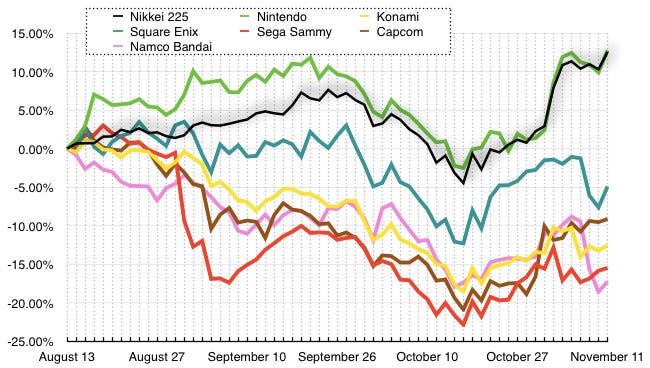

Here's the graph for traditional publishers in Japan, and as you can see, it doesn't make for particularly happy reading. In spite of the strong performance of the Nikkei in recent weeks thanks to the Bank of Japan's decision to throw Yen around like there's no tomorrow, most Japanese publishers have had a miserable time of it - dating all the way back to early September, when prices first slumped, with little sign of recovery since then. Indeed, the only publisher in the bunch that has really recovered thanks to the Yen's weakness is Capcom, and even then it wasn't enough to reverse the decline of the previous couple of months.

What's going on here, then? I think the most likely explanation for this poor performance actually has very little to do with videogames and everything to do with gambling. Many of these companies, especially Sega Sammy, don't just publish videogames; they also operate "game centres" in Japan, chains of arcades which have over the past decade or two become much more focused on gambling-style machines than on actual arcade games. Some of them (again, Sega Sammy in particular) also have large investments in Pachinko and Pachislot parlours, which are a form of gambling-style game that's insanely and inexplicably popular with many Japanese people. However, Japan has strict rules forbidding most forms of gambling; you'll note that I said "gambling-style games", not outright "gambling". There are shady ways around this that many Pachinko parlours will employ, but in general, arcades are restricted to providing games that give users the buzz of gambling without the actual payout.

Up until summer, that looked like it was about to change, with the government seemingly set to legislate for the construction of licensed casinos - but that legislation has been gradually watered down throughout the autumn, with the number of casino sites and their locations being reduced, then an amendment to make access to the casinos illegal for Japanese nationals (so they would only be for tourists), and finally the strong likelihood that the government is going to drop the legislation entirely. Japanese game companies like Sega would probably have hoped to make a killing from the legalisation or partial legalisation of actual gambling; with that off the cards, their stocks have slumped. That slump has probably taken some innocent victims along with it (game companies who had nothing to do with this business in the first place), but that's not unusual; investors often withdraw from an entire sector rather than a specific business when they're placing their bets.

How, then, did the Japanese mobile and social companies fare through all of this? With the exception of DeNA, not much better. DeNA has had a great quarter, posting much stronger results than expected thanks largely to the excellent performance of Final Fantasy Record Keeper, a new title it recently launched with Square Enix (whose share performance, you might have noted, was notably better than the other publishers in the previous graph). The firm is still making far less money than it was a year ago, but it's showing signs of growth and rejuvenation which is precisely what the stock market wants from its companies.

DeNA's major rival, Gree, has been pursuing a similar strategy - particularly with regard to moving its titles away from browser-based games and towards native games - but lacking in a game on the scale of Final Fantasy Record Keeper, it's not managed to grab the attention of investors to the same extent. A solid spike in October stemmed from a partnership with insanely popular messaging application LINE, while good results in the past few days gave a little spike at the end, but overall the company's performance hasn't matched DeNA's. All it would take would be one really huge game launch, though, for this situation to reverse.

Finally on this chart, GungHo remains a lesser known company, but it's the publisher of Puzzle & Dragons (the world's largest grossing game in 2013, fact fans) and the firm that, along with its parent company SoftBank (a mobile phone network), bought Clash of Clans creators Supercell. It's not had a great quarter; in fact, it's had a very tough quarter after a reasonably decent 2014 up to that point. The reason for GungHo's difficulties is likely related to the launch of a number of high-profile mobile titles in the past few months - most notably Monster Strike, but a host of other heavily marketed titles, mostly RPGs, have been storming up the App Store charts of late. Puzzle & Dragons is still an enormously profitable and popular game, but it's getting long in the tooth and GungHo has yet to release anything that could credibly take its place. Similarly to King, then, the company finds itself in the shadow of its own enormous hit title, and harshly judged on its ability to repeat its success.

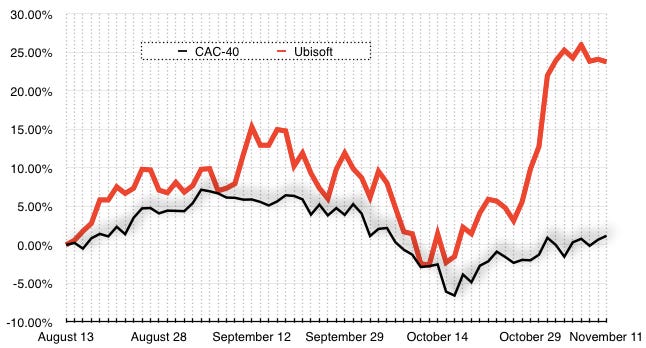

Finally, then, let's take a look at the only European stock of any particular note - European publishing holdout Ubisoft, which is listed on the Paris stock exchange and thus needs comparison with the CAC-40 index.

A very solid few months for Ubisoft, then, with the company's enormous spike in performance in late October being down to the reiteration of its financial guidance for the rest of the year. Ubi is on track for a blockbuster year, with sales in its winter quarter expected to be 40 percent higher than last year - yet more growth for a company that's gone from strength to strength over the past decade, at least financially. Of course, stock prices reflect sentiment so it's worth noting that critical reaction to the latest Assassin's Creed game has been very mixed, veering towards the negative, in sharp contrast to the high anticipation for the title; this may hurt Ubisoft's share price in the coming days and weeks, although should sales figures hold up, the damage will be minimal. Still, the franchise is definitely the feather in the publisher's cap and will need to be carefully managed, not merely milked, if the company is to continue to enjoy the confidence of its investors.