Money Games: Online, Mobile, China and More

Digi-Capital's Tim Merel on the fundamental shifts in games investment for 2011

After a short break, Digi-Capital MD Tim Merel returns this month with his regular column looking at investment in the games sector.

This month he takes us through his recently updated Global Video Games Investment Review, looks at the shift towards online and mobile, why China (not America) may dominate games globally, and why 2011 is the year to invest for growth or look for the nearest exit.

Having just published our 2011 Global Video Games Investment Review (available to read here), and spoken at a fascinating GDC in San Francisco, it's a good time to talk about the videogames investment trends which are transforming the industry.

The Acceleration and Fundamental Shift to Online/Mobile Investment

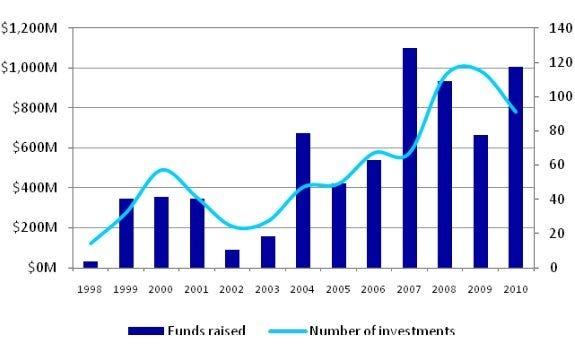

As we anticipated in our 2010 Review, videogames activity accelerated and changed fundamentally during 2010. VC games investment approached 2007 levels in 2010 in terms of funds raised, although the number of investments declined. The top ten investments accounted for around 60 per cent of total games investment in 2010, with a fundamental shift to online/mobile games company investments.

However general VC market weakness and limited knowledge and relationships across complex, fast moving online/mobile games sectors still make generalist VC games investment challenging.

Global Video Games Private Placements

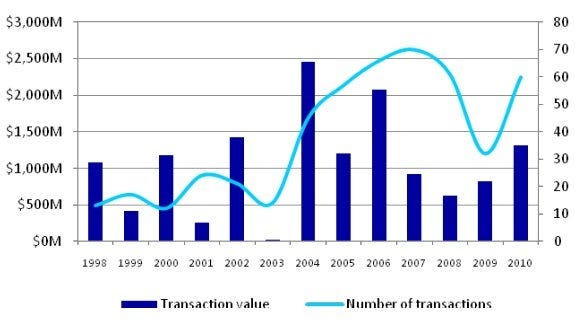

Global Video Games Mergers and Acquisitions

Major console publishers continue to struggle to adapt to online/mobile, with a focus on existing large console games franchises rather than new intellectual property, as the console games market is flat to down, with declining profitability.

The reason for this challenge is that major publishers' core competencies focus on management of $20 million-plus serial, high risk, complex developments, launches and commercialisation. Online/mobile games require rapid, multiple, small scale parallel development platform investments, completely different to major publishers' business cultures, so they are not driving online/mobile games investment.

Similarly, major publishers are wary of large scale online/mobile video games M&A in early stage, fragmented markets where market dominance is not yet clear.

Quality investment demand still exceeds supply, with high quality, high growth (100 per cent annual revenue growth, 20-50 per cent operating margin) online/mobile games companies seeking investment to accelerate growth.

Outside the major investment deals, online/mobile games companies still find it challenging to find high quality investors despite major publisher/media consolidation (Electronic Arts/Playfish $400 million, Disney/Playdom $763 million, DeNa/ngmoco $400 million, Tencent/Riot est $350M-$400 million, Shanda/Mochi Media $80 million).

This isn't to say that good deals aren't being done, but that industry growth and competition could accelerate even faster with more high quality investors in the system.