2023 UK game sales "holding the fort" compared to 2022, but still show signs of growth

Sparkers analyst consultant Sam Naji explores how full game UK sales display signs of robustness in consumer spending

Sign up for the GI Daily here to get the biggest news straight to your inbox

2024 so far has been challenging in the industry. This is a good time to take stock of last year's performance to gauge demand-side conditions and what direction consumer spending is going in the UK when it comes to full games (games that are paid for upfront).

With the complete set of UK retail and GSD tracked digital data in for 2023, we can reflect on some good news that the year turned out quite positive:

- Combined physical and dsgital unit sales for 2023 was 3% higher compared to 2022.

- Average price increases in new games increased by 14% between 2021 to 2023.

- Unit sales for digital full games continues to grow as a share of the total UK market, but the transition to digital has slowed down.

When it came to video game spending in the UK during 2023, unfavourable economic headwinds did not dampen spending when it came to full video games.

In this analysis, I will use Game Sales Data (GSD) to take a snapshot of the UK's full game market during 2023. GSD provides a holistic view of the video game market, combining both physical disc format games bought at retail as well as digital code on receipts bought at retail and games directly bought from the PlayStation Store, Xbox Store, Nintendo eShop, and all major PC digital stores, including Steam, Epic Games Store, Ubisoft Store, EA Play and so on.

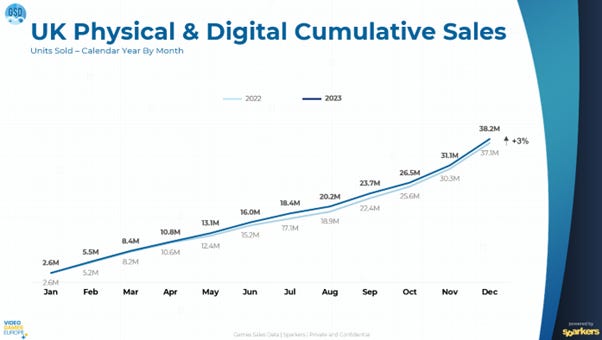

From the highest perspective, full-game unit sales came to 38.2 million units in 2023, an increase of 3% compared to 2022.

Between January and April in both 2022 and 2023, the two years almost matched each other in combined unit sales. Each year saw the release of successful titles in the early months. In 2022, Elden Ring, Lego Star Wars: The Skywalker Saga, and Horizon Forbidden West all had successful releases and in 2023, Hogwarts Legacy, Star Wars Jedi: Survivor, and Resident Evil 4 also performed well with their respective release. It was only from May that 2023 began to outperform 2022.

In Chart 2, the shift towards stronger sales in 2023 occurred in May with the release of Nintendo's The Legend of Zelda: Tears of the Kingdom. Strong sales for Nintendo's game were further enhanced in June when Activision Blizzard released Diablo 4. For comparison, the combined sales of The Legend of Zelda: Tears of the Kingdom and Diablo 4 in their respective first weeks on the market were five times higher than the combined sales of last year's F1 22 and The Quarry, the two best-selling new releases in May and June of 2022.

For the second half of the year, the margins in unit sell-through between the two years got tighter. In September, EA Sports FC 24 (2023) sold 8% fewer units than FIFA 23 (2022). When Call of Duty: Modern Warfare 3 released in November 2023, it sold 8% fewer units compared to the October 2022 numbers for Call of Duty: Modern Warfare 2. These losses were somewhat offset with the release of Starfield in September 2023, plus Assassin's Creed Mirage and Super Mario Bros. Wonder in October 2023.

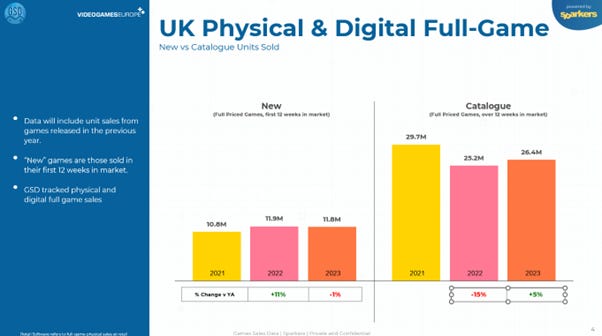

In respect to new game sales compared to those of catalogue game sales, 2023 performed strongly. New games are those games that sold in their first 12 weeks in market, the time when publishers could maximise returns based on highest demand before any price discounts. Catalogue sales here are for those games which have been in market over 12 weeks since release.

Unit sales for new games reached 11.8 million units in 2023, a marginal decline of 1% compared to 2022 but 10% higher when compared to 2021. Unit sales for catalogue game came to 26.4 million units, an increase of 5% since 2022, but 11% lower than in 2021.

Video games still represent one of the best entertainment values for the money. As spending becomes tighter, the value proposition offered by games has become increasingly more attractive. Whether games can be described 'recession proof' is debatable and the jury is still out; this is a topic I covered in a previous article on GamesIndustry.biz.

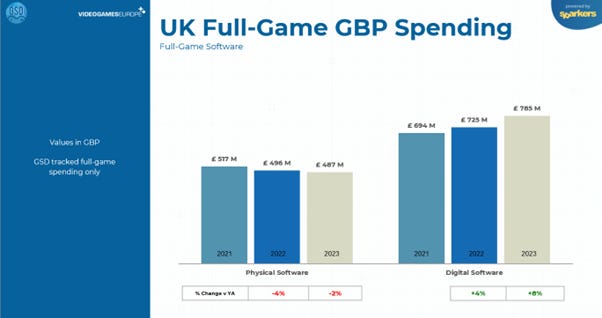

Regardless, indications from this year show a strong resilience against a decline in spending. In Chart 4, we see spending on full games for both physical and digital formats came to £1.27 billion, making for an increase of 4% compared to 2022 and 5% higher when compared to 2021.

The increases are coming from digital full game spending which increased by 8% since 2022 to reach £785 million by 2023. Although physical disc spending has continued to slip since 2021, the rate of the decline had slowed. Between 2021 and 2022, spending declined by 4% to £496 million but between 2022 and 2023, spending declined by just 2% to £487 million.

It would be easy to state that physical game spending is dying as digital spending grows, but whether sales increase or decrease depends greatly on how one is analysing the business. For example, it depends on whether the investigation captures the entire full video game market or just new game sales.

Other factors include whether one is investigating games that released on the digital format only (such as Alan Wake 2) or whether games got an early digital release compared to their physical disc counterpart (such as EA Sports FC 24 and Call of Duty Modern Warfare 3). All these factors can contribute to favour the digital format away from physical disc sales.

Some of the increase in spending between 2021 and 2023 can also be attributed to the increasing average price of games. The question of whether the prices of games today are more expensive than in the past was covered in some depth by another GamesIndustry.biz article, Are Video Games Really More Expensive?, but the fact remains that unit sales increased despite the higher price rises.

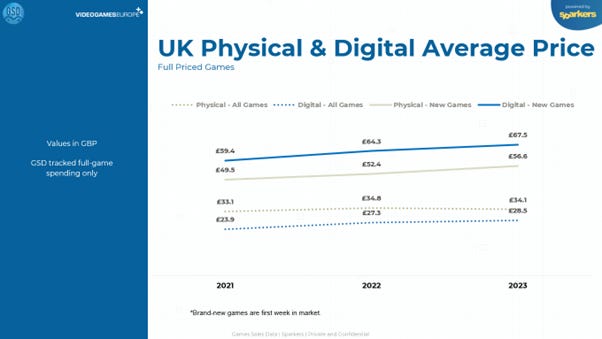

Chart 5 illustrates the increases in the average prices of games in the UK. Prices for physical boxed brand new games (games sold in their first week on the market) went from an average of £50 in 2021 to £57 in 2023. For brand new games in the digital format, the average price of £59 in 2021 increased to £68 by 2023. This represents an increase of 14% respectively for both formats.

The impact of increasing game prices didn't just affect brand new games; it also impacted the average price for all video games in the market. The price for all games in the physical disc format increased from £33 in 2021 to £34 by 2023. The price for all games in the digital format increased by 19% since 2021 to £29 by 2023. It is encouraging to see that the video game price increases have not dampened additional unit video game sales, and it speaks volumes about the desire of UK gamers to continue buying games, even in these uncertain times.

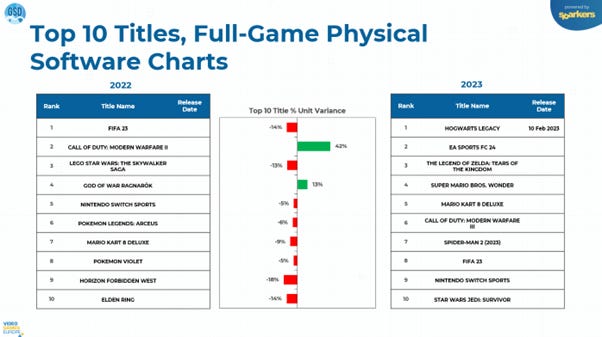

The growing appetite for video games in the UK is evident when we examine the top ten best-selling games by units during 2023, with the physical top ten shown in Chart 6 below.

Two games experienced an increase in unit sales during 2023 compared to their ranked counterparts from 2022. The 42% increase in sales in the second ranked game for 2023, EA Sports FC 24 (over the units that Call of Duty: Modern Warfare II pulled in as the second ranked game of 2022) was able to offset the losses elsewhere among the top ten.

In 2023, the top ten ranked games sold just 2% fewer units compared to the top ten titles of 2022.

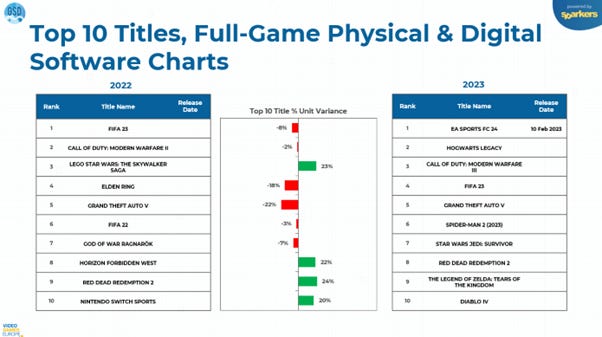

Interestingly the 2% variance in unit sales between 2023 and 2022 was also evident when comparing the top ten titles for both physical and digital formats combined, as shown in Chart 7. In 2023, only four games beat their ranked counterparts from 2022. One partial explanation for this downturn could be the fact there was an increase in spending for cheaper catalogue titles.

In summary, GSD-tracked data for 2023 UK full video game sales can be best described as holding the fort. Although there was 3% growth in unit sales and 5% growth in spending, UK consumers did not gravitate to the new releases for 2023 with a strong sense of enthusiasm, opting instead to bolster sales on catalogue and older games.

The 14% increase in average price increase for new games in the last two years, whether in the physical or digital format, most probably has affected some consumer behaviour to wait for price reductions of these games further down in time.

Signs are that 2024 could be a repeat of 2023, with fewer tentpole releases expected in the first half of this year, compared to 2023 or 2022. Being an optimist, the latter half of the year should hopefully offset any declines during this early period.

If you are interested to know more about Sparkers and GSD and how they can help you with video game analytics please visit the website sparkers.com or contact info@sparkers.com.