Stock Ticker: 2011 In Review

Format holders, publishers, retailers - who won and lost on the global stock markets last year?

It's customary, around the end of one year or the beginning of the next, to write articles declaring the "winners" and "losers" of the year. The games press, in particular, loves this tradition - perhaps it's something to do with the nature of what we're writing about, but it seems that games writers are obsessed with working out who has "won" or "lost" even the most non-combative of situations. Who won E3? Who lost GamesCom? Who walked away with TGS? Who took a beating at EG Expo?

The reasonable response to most of those is probably "who cares?", but there's one game which every company in the industry definitely wants to win - and that's the international high-stakes roulette wheel that is the stock market. In fact, much to the chagrin of consumers and creatives alike, the realities of modern market capitalism mean that the games business (like every other business) picks its top executive staff not for the ability to produce great products, but for their ability to pander to the markets - managing expectations, massaging figures and only concerning themselves with great videogames when that's a vital part of the market strategy (and sadly, it sometimes isn't).

As such, it seems appropriate to look back at 2011 a little more coldly than most retrospectives of the year have done so far, and look at how the industry's top companies performed on their respective stock markets. One word of warning is due; these figures aren't necessarily representative of anything about the firms' actual financial health, the quality of their products or even their growth. Stock markets don't trade on sensible things like that. They're driven by an insatiable desire for growth which deplores stability, as well as by powerful currents of rumour and sentiment. A stock market collapse doesn't necessarily mean you're going bust - but it probably means that you're going to have a radical change of top management very soon.

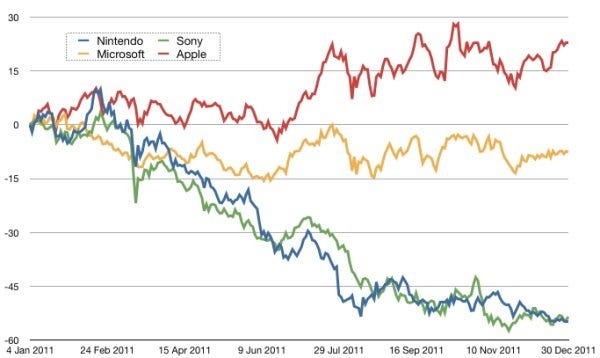

With that being noted, let's look first to the industry's behemoths - the platform holders. Here's how they stacked up in 2011:

This graph shows some pretty clear water between the Japanese duo of Nintendo and Sony and their American rivals at Microsoft and Apple (whom I've included essentially as a platform holder representative of the wider mobile market - I think we're now long past the point of there being any debate about whether Apple directly competes with gaming platform holders or not). However, it's not exactly a fair graph, for a few reasons.

Firstly, we're only interested in games, and not all of these companies are equally engaged with games. For Nintendo, games are 100 per cent of its business. For Sony, it's a large and vitally important business, but not even half of the whole enterprise in turnover terms. Microsoft's Xbox business is absolutely dwarfed by the scale of Windows and Office. Apple, meanwhile, probably wouldn't even consider itself to be in the business of games most of the time, even though it does increasingly promote its iDevices as gaming platforms, and takes home a healthy 30 per cent share of the increasingly massive iOS gaming market.

Compared to the ongoing struggles with Apple and Google, Microsoft's battle with Sony barely registers with most investors

So essentially, while Nintendo's performance is directly reflective of weakness in its games division, and Sony's also reflects uncertainty about the PlayStation business to a degree, the chances are that Microsoft and Apple's figures don't really bear much relation to their prowess in gaming. If the Xbox business collapsed tomorrow, it would be seen more as a strategic loss than a real financial hit for the company - it's hard to say how the stock market would react, but compared to the ongoing struggles with Apple and Google, I'd wager that Microsoft's battle with Sony barely registers with most investors.

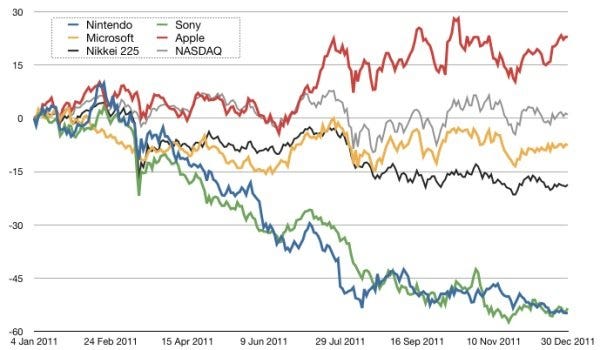

There's a second unfair factor about this graph which we can do something about, and that's the fact that these companies trade on different national stock markets. Financial conditions in Japan and America were rather different this year, as you can see reflected in the relative performance of the Nikkei 225 (Japan's stock market index) and the NASDAQ (America's tech stocks index). Let's plot them on the graph:

Here we can see a slightly sobering reality - although the Nikkei is down for the year, Nintendo and Sony deeply underperformed compared to the wider Japanese economy. In the USA, while Apple outperformed the NASDAQ comfortably (and is still considerably undervalued, going purely off financial indicators from the firm's results, suggesting that either the market is worried about Apple's future or that it's just not caught up to the firm's incredibly rapid growth yet), Microsoft underperformed the index somewhat, having a year best described as "tepid".

Don't take Nintendo and Sony's figures as an indication that Japan as a whole is in trouble, though. I'll come back to those figures later on - there's good news for Japan, albeit arguably even worse news for the platform holders, when we look at a broader set of stocks.