Stock Ticker: Sony soars, Microsoft slumps and EA reclaims its crown

Platform holder fortunes are reflected in their 2015 performance to date, while Japan's Gumi hits the skids after its billion-dollar IPO

With many of the games industry's largest companies reporting financial results or updating their official earnings forecasts over the past two months, it's a good time to check in on how the industry's stocks are performing. If you read our 2014 Year in Review article back in December, you might recall that the best-performing stock of last year was Electronic Arts, which doubled in value in 2014, while Take-Two, Ubisoft, Square Enix, Sony and Apple also had very strong performances, each of them rising by 30 percent or more over the course of the year. At the other end of the spectrum, Sega Sammy had a disastrous 2014, as did Zynga, with both firms slumping by 40 percent in value; while Puzzle & Dragons publisher GungHo was the least impressive of an overall poor showing for Japanese mobile game publishers, down some 35 percent in value, with Gree and DeNA both also dropping 30 percent over the course of the year.

So, how have last year's winners and losers fared over the course of 2015 thus far?

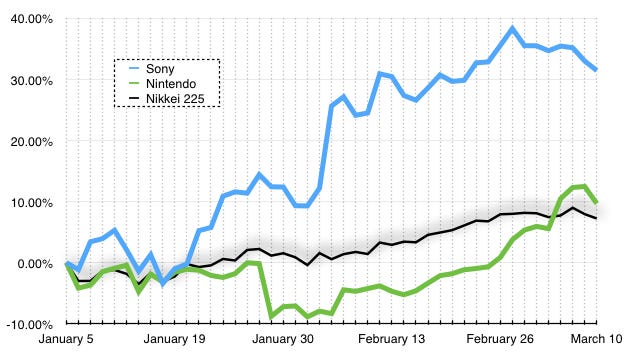

We start as ever with the Japanese platform holders (Japanese and US companies are charted separately in these articles since it's hard to compare like-with-like across the ocean, stock prices being inevitably hugely influenced by local economic issues). Perhaps unsurprisingly, it looks like last year's pattern is being repeated. Sony continues to soar - it's added another 30 percent boost to its rise in price last year, comfortably beating the Nikkei thanks largely to a healthy boost at the start of February when the company announced that it's on-track to beat its own targets for revenue and income this year. Over the past 12 months, Sony's stock has risen some 80 percent - the last time its shares traded at this level for any sustained period was before the 2008 financial crisis.

Nintendo, meanwhile, suffered a slump at the end of January when it missed its nine-month targets and revised its full-year targets downwards; but things picked up through late February, with the US and EU launches of the New 3DS hardware and the remade Legend of Zelda: Majora's Mask helping to focus attention onto the company's successful handheld devices and away from the under-performing Wii U. This most recent little "pop" in the share price leaves Nintendo up over 5 percent in value over the past 12 months, although it's still a poor investment; over the same period, the Nikkei index overall has jumped 23 percent.

"EA is also back to being the industry's top third-party publisher in terms of its value, with its market capitalisation overtaking Activision Blizzard's to reclaim the top spot"

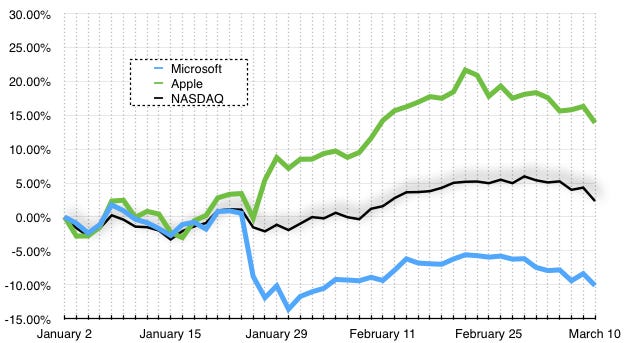

Across the Pacific Ocean in Seattle, the other major platform holder is having a bad 2015 so far, with Microsoft by far the worst performer of the three major console companies. That's not really attributable to Xbox, although the console's weak post-holiday performance hasn't exactly done the share price any favours either; rather, it's all down to a big slump in mid-January, when new financial data from the company showed a big drop in revenue from the Windows operating system which gave the markets serious jitters. Since late January, Microsoft has tracked the NASDAQ index fairly closely, so there haven't been any more upsets, but if Windows revenue is under threat then the need for CEO Satya Nadella to clarify and demonstrate his vision for the future becomes all the more pressing. What that means for the Xbox division, often cited as an odd-man-out in the firm's largely business-focused plans and now seemingly going through yet another leadership reshuffle, is anyone's guess. By contrast, Apple managed to pull another 15 percent in share price growth out of 2015 so far, in spite of now being the world's most valuable company; the contrast with Apple (and with Google, also booming but not included here as it's arguably less relevant as a games platform holder) won't be doing anything to make life easier for Microsoft's top management.

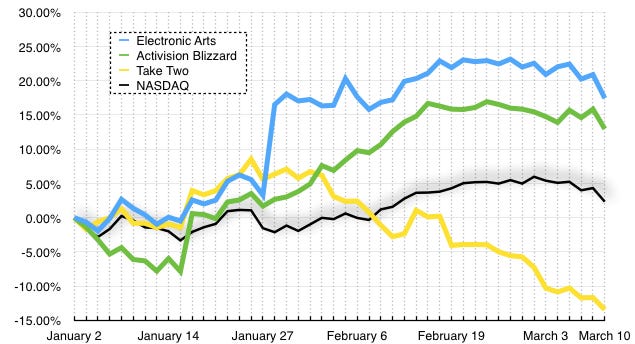

Staying in the United States, here's a glance at how the region's publishers have done so far in 2015 - including last year's top performer, Electronic Arts, which has continued its fantastic run into another year. EA is now up over 90 percent in 12 months, and its share price is close to the record highs it achieved between 2004 and the financial crisis in 2008. In fact, since EA's shares bottomed out and started climbing in mid-2012, the company's value has grown over 350 percent - in the same period of time, the NASDAQ is up by only 60 percent. Incidentally, EA is also back to being the industry's top third-party publisher in terms of its value, with its market capitalisation overtaking Activision Blizzard's to reclaim the top spot. Both firms are also more valuable than Nintendo right now - quite a reversal of fortune, given that Nintendo was Japan's most valuable company at the height of the Wii era.

EA's boost in late January came from better than expected earnings, with investors also liking the success of Dragon Age Inquisition and of the firm's mobile gaming line-up. Activision, which has also had a good year so far, didn't see much response to its own positive earnings in early February, but that may be because investors were already aware that it was going to beat targets - it announced that Call of Duty and Skylanders had outperformed expectations in a press release in mid-January, where you can see a quick hop in share price. Take-Two, meanwhile, has had a very tough couple of months on the markets, but that that's largely just the share price rebalancing itself after a brilliant 2014 - and perhaps coming to terms with the reality that, with GTAV now out the door on the next-gen consoles, Take-Two's results for this year will inevitably be weaker than last year's, since it doesn't have anything to match GTA's performance on its release slate.

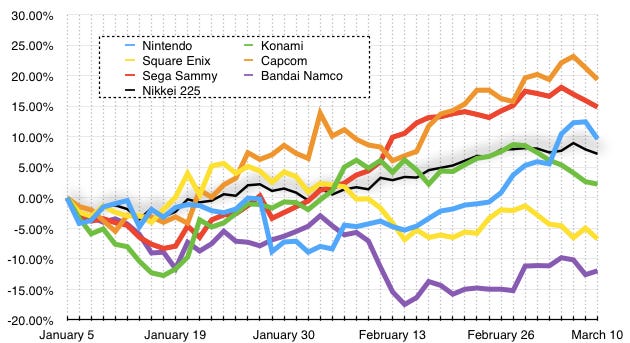

Swinging back across the Pacific to look at Japan's publishers, we find quite a mixed offering. Nintendo (as previously mentioned), Sega Sammy and Capcom are beating the Nikkei 225 index; Konami, Square Enix (last year's top performer) and Bandai Namco are all down. For Bandai Namco, the worst performer of the bunch, the markets didn't take well to the firm's earnings report in mid-February; the company did better than last year in almost every respect, but failed to live up to expectations (which may have been set too high due to the near-ubiquity of Yokai Watch in Japan right now). Square Enix, meanwhile, found itself in a similar position to Take-Two in some ways, with the share price decline largely attributable to rebalancing after a strong 2014; much of that was focused around the February announcement that Square Enix would hit (rather than exceed) its previously announced targets.

"Sega Sammy is barely a videogames company any more, but as long as the Sega IP catalogue remains useful and valuable to the firm's other enterprises, any talk of spinning off the videogames businesses (including the excellent overseas offices and studios) will be very premature"

At the other end of the spectrum, Capcom investors are largely happy with the company's progress in terms of cost-reduction and moving over to digital distribution, with Monster Hunter 4 Ultimate being the stand-out title for the company right now. Sega Sammy's story, meanwhile, is an interesting one. The company's results are increasingly divorced from the videogames business - last year it suffered hugely from the will-they, won't-they drama surrounding the Japanese parliament's decision to pass legislation permitting the construction of casinos in Japan (in the end, the legislation was shelved, but may be revived later this year). This year, Sega Sammy has popped up partially on the realisation that it may have been undervalued last year, and partially on the positive news surrounding a co-venture to construct casinos in South Korea, a country widely expected to become a major centre for gambling resorts in the next few years. Where does Sonic figure in all this? He doesn't, really; Sega Sammy is barely a videogames company any more, but as long as the Sega IP catalogue remains useful and valuable to the firm's other enterprises, any talk of spinning off the videogames businesses (including the excellent overseas offices and studios) will be very premature.

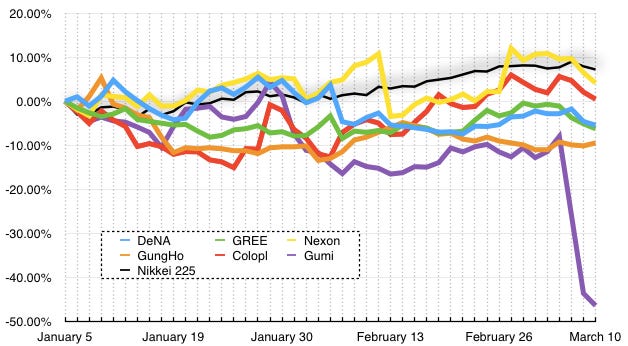

At the other end of the Japanese market, looking at the country's mobile publishers, we see the most dramatic chart of this round-up; look at the state of Gumi! The company, which publishes hit mobile game Brave Frontier in Japan, only launched on the stock market last December; at the start of this month, it received the mother of all hangovers from its IPO, with the price crashing hard after it announced that its expected $10.6 million profit for the year ending April 30th will actually be a $5 million loss. The change in forecast is largely down to the underperformance of Brave Frontier outside Japan, and a general failure to execute on an overseas strategy; the sheer magnitude of the price drop is likely down to the perception that completely reversing your full-year forecast only two months before the end of the year suggests, at best, a complete failure of oversight.

No other Japanese mobile publisher did particularly well either; Nexon, which was last year's top performer, is just about tracking the Nikkei index, but the likes of GungHo, DeNA and Gree are extending their losses, albeit slowly, as each of them struggles to come up with a convincing plan to grow their business in the coming years (and, in the case of GungHo, a convincing way to show the world that Puzzle & Dragons wasn't just a happy stroke of luck). After lots of up-front enthusiasm, there's a sense that Japanese investors (and, indeed, investors everywhere) are concerned that mobile gaming is a bit of a crapshoot, with the real mega-hits being utterly unpredictable and impossible to repeat.

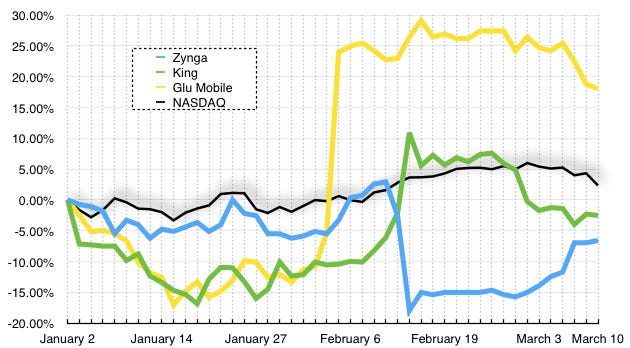

That sentiment probably has a lot of relevance to our final chart as well; the US' three major publicly listed mobile game publishers. I've written before about the curiosity in Zynga and King's share prices in mid-February, where Zynga's rising revenues were punished by a plunging share price while King's falling figures were welcomed with a major boost - but the reasons are actually quite clear, since Zynga continues to be slow at executing a successful move to mobile, while King has done a good job of building up other titles to replace the rapidly declining revenues of mega-hit Candy Crush Saga. As it turned out, this wasn't a long-term effect anyway; by the start of March, both firms were pretty much back to their original performance levels.

The stand-out here, of course, is Glu Mobile, which soared at the end of January partially thanks to good financial results, but mostly thanks to the announcement that the company behind the wildly successful Kim Kardashian mobile game has secured the rights to make a game based around Katy Perry. Investors may be concerned about the ability of mobile companies to repeat their hits (this also explains why King's demonstration that it's still capable of maintaining revenues even if it can't re-bottle the lightning that created Candy Crush Saga was so welcome), but licensing incredibly famous people's images and using them to extend franchises that are already tried-and-tested seems downright sure-fire. Given the volatility of the mobile market, I wouldn't be one bit surprised to see this sure-fire thing completely mis-fire; but for now, Glu's share price is riding high, albeit from a pretty low starting point.