Nintendo, Capcom top Japan's game stocks in 2015

Nintendo and DeNA's deal dominates trading in Japanese game stocks, as the market takes a cautious approach to mobile game stocks despite strong growth.

Editor's Note: This is one in a series of year-end content to be published daily leading up to Christmas that includes analysis, opinion and insights into the biggest news and trends of 2015.

Yesterday, we saw how game publisher stocks in the US and Europe have soared in 2015, led by Activision Blizzard, EA, and rumours of an acquisition bid for Ubisoft. The underlying reasons for the boom are all about investor confidence in games as a sector; the stellar performance of the new generation of consoles has put to bed fears that the hugely profitable console sector was facing collapse, while there's growing faith in the mobile sector as a sustainable business sector, not merely a fad or a flash in the pan.

Today we turn our attention across the Pacific Ocean to Japan, where the lion's share of the world's publicly listed game companies are to be found on the Tokyo Stock Exchange. Many of the same fundamentals apply in Japan - even more so with regard to the mobile sector, an industry where Japanese and Japanese-owned companies are thoroughly dominant - but the Japanese economy itself, and thus the stock market fundamentals, are very different from the US and Europe. The market has grown remarkably since late 2012 and is now at heights last seen 15 years ago - but it's unstable at the top, and contradictory economic data and conflicting interpretations from economists have caused the Nikkei 225 to crash sharply a couple of times this year. As such, we won't be comparing any US stocks to Japanese stocks in this round-up; the fundamentals are simply too different for any useful data to be gleaned.

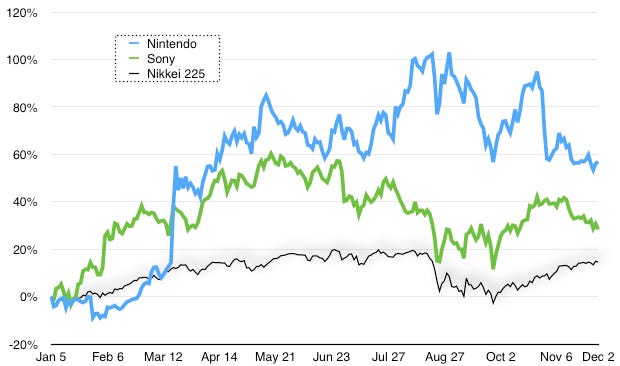

We start with Japan's two platform holders, Sony and Nintendo. Given the extraordinary performance of the PlayStation 4, it might be something of a surprise that Nintendo has had a much better year on the markets than Sony - but there's a story behind that. The performance of Nintendo peaks in August, as the markets responded to the success of Splatoon - proving the firm's ability to create brand new multi-million selling IP - but it first soared in mid-March, and experienced a sharp decline in early November, effectively defining the shape of Nintendo's stock price movement this year. That rise in March is the announcement that Nintendo plans to work with mobile publisher DeNA to release games for smartphones; the drop in November was the announcement that the first games under this partnership have been delayed. Essentially, everything else on Nintendo's graph - even the Splatoon-inspired spike - is just noise; all the stock market cared about this year was the potential of Nintendo IP on mobile devices.

By contrast, Sony's figures - while comfortably outperforming the Nikkei 225 - were fairly unremarkable. Shares rose nicely at the start of the year as the extent of the PS4's holiday sales performance became clear, but have flatlined and even declined slightly since then. The enormous success of Sony Computer Entertainment can't allay the markets' concerns about Sony's wider business. While PlayStation is becoming an increasingly vital part of the company, the turnaround strategy being executed by CEO Kaz Hirai is still a work in progress, and ongoing reports of disgruntlement among some of Sony's senior statesmen make investors a little nervous. It's the best year in a while for Sony's stock, but the company still has a lot to prove.

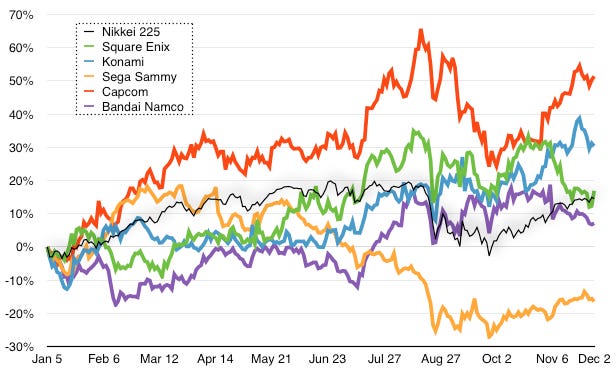

Looking now at the rest of Japan's "traditional" publishers, we can see that most of them performed reasonably well in 2016 - although the soaring success of America's top publishers wasn't replicated across the ocean. The only Japanese publisher that desperately underperformed the market was Sega Sammy, whose woes are largely down to factors outside of videogames; the bulk of the company's revenues are down to Pachinko and Pachislot - Japan's "it looks like gambling, it smells like gambling, it tastes like gambling, but we're legally required to say that it's definitely not gambling" habit of choice. The problem is that these games are slowly falling out of favour with consumers; nobody's quite sure if that's down to a generational shift, or the sharp decline in Japanese real incomes in recent years, or a bit of both, but it's certainly being felt on Sega Sammy's bottom line. Combine that with ongoing dithering over legislation permitting casinos to open in Japan and Korea alike, and the whole gambling (or "sort-of gambling") side of Sega Sammy's business is clearly on shaky ground.

"If [Nintendo's] mobile titles fail to impress, expect the share price to tank; there's a hell of a lot riding on whatever Nintendo and DeNA are brewing up"

Square Enix and Bandai Namco turned in fairly unremarkable results this year, broadly in line with the Nikkei 225's own movements, while keen news-watchers may be surprised to see Konami doing exceptionally well, almost doubling the gains of the broader index. The company may have lurched from debacle to disaster and back to debacle again in the specialist media this year - capping it all off with the genuinely cringe-worthy and infantile decision to ban Hideo Kojima from accepting awards for his own game, MGS5 - but the move towards a mobile-first strategy has been broadly welcomed by the stock markets, making Konami into one of the best performing game stocks in Japan this year. Way out in front, though, is Capcom; the company is smaller, in market capitalisation terms, than many of the others so it's easier for it to make significant gains, but regardless of that, it also executed extremely well this year and the markets seem particularly excited by the ongoing push to get the Monster Hunter franchise established on mobile.

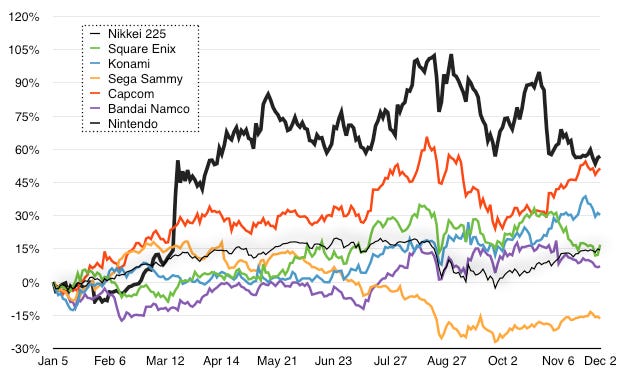

We say Capcom is out in front; actually, the top performer isn't on this graph. If we take Nintendo's figures from the previous platform holders' graph and superimpose them on the publishers' graph (Nintendo being, after all, far and away the biggest software publisher in Japan), we see who the real winner among the publishers is.

Again, that Nintendo line is really all down to market excitement about the company going mobile. If its mobile titles fail to impress, expect the share price to tank; there's a hell of a lot riding on whatever Nintendo and DeNA are brewing up in their development studios.

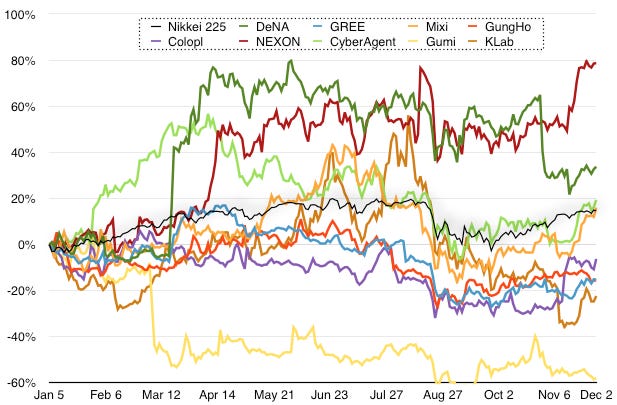

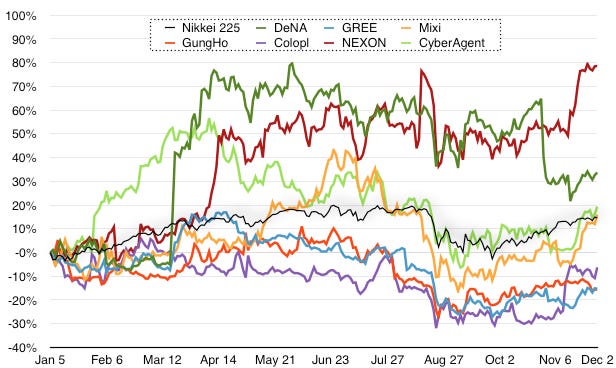

Turning our attention to mobile- and digital-only firms, we get a graph which, honestly, we could find no way to render more legibly.

Yes, there are a hell of a lot of publicly listed mobile publishers in Japan - and in fact, that's not even the full set, as we left off a couple of companies with very small market caps and quite obscure, local market specific games. We'll tidy this graph up a little more in a moment; for now, turn your eyes to Gumi, the gloomy looking line bouncing along in the negative numbers all year.

Gumi had its IPO last year, and in the early part of 2015 it dramatically revised its financial figures downwards, causing the stock to tank. The brightly optimistic and clearly entirely wrong figures being touted around the time of the IPO seemed all-too-convenient to many investors, and it's going to take a hell of a lot of work for the firm to regain the confidence of the markets.

In the interests of legibility, we've created a second graph for mobile stocks - this time excluding any company with a market cap of less than $1 billion (about ¥120 billion). Interestingly, that leaves GREE - often perceived as a giant in the Japanese mobile industry - as the smallest company on the chart, and a significant drop next year could see it fall below the billion dollar mark. The company has lost three quarters of its value since its peak at the start of 2012, and this year saw no halt to the decline. It's still in the billion-dollar-club for now, but whether it can stay there next year will depend on the firm finding a bold new strategy that impresses investors.

This chart is still a little messy, but it's a bit easier to read the highlights now. The top performer is Nexon, formerly a dedicated operator of online and massively multiplayer games, whose entry into the mobile space has taken an interesting form; it's largely positioned itself as the go-to company for developing and operating mid-core games using other firms' IP. It's presently working on a mobile version of Square Enix's venerable and much-loved MMORPG, Final Fantasy XI; this is the kind of project that's typical for Nexon, having previously worked on IP like EA's FIFA and Valve's Counter-Strike. While the downside of such a work-for-hire approach is that the company ends up owning little or no valuable IP of its own, investors are clearly impressed by the revenues this generates, and the illustrious and growing list of top companies entrusting Nexon with their titles.

"Japan's mobile companies have plateaued in valuation in 2015; the markets are in holding formation waiting to see what happens next"

After Nexon, the next best performer is DeNA - and this is the mirror image of what we saw on the platform holder chart, with DeNA's shares also soaring when its contract with Nintendo was announced, and slumping when the delay to Nintendo's mobile games was revealed. Despite the size of the two companies involved, it's clear that the markets presently view them as somewhat symbiotic; if the Nintendo/DeNA mobile titles don't do well, both companies will undoubtedly suffer badly on the Tokyo Stock Exchange as a result.

Further down the chart, just about keeping pace with the Nikkei 225 index (and in some cases somewhat underperforming it), we find a bevy of the world's top mobile game developers and operators. Mixi, creators of the world's present top-grossing mobile game, Monster Strike, just about edges out the index - it experienced a severe downturn in its valuation when Apple briefly pulled Monster Strike from the App Store over the summer, citing the company's policy of giving away a lot of premium items and currency with voucher codes in magazines and so on as a violation of App Store policy. Coinciding with the broader slump in the Nikkei in late August, this gave Mixi's share price a blow from which it has yet to entirely recover - although with the company trading at historic highs since mid-2014, it's unlikely to be overly concerned.

In fact, that's broadly the story of a number of these companies, including Colopl (developers of White Cat Project) and CyberAgent; while their share prices have coasted in 2015, they've been coasting near historic highs for both companies. This does suggest that investors are concerned about their potential for future growth (perhaps noting that few of the world's top mobile firms, including Puzzle & Dragons operator GungHo, have been able to re-bottle the lightning that gave them their break-out hit titles), but not concerned enough to sell the stocks they're holding. Japan's mobile companies have plateaued in valuation in 2015; the markets are in holding formation waiting to see what happens next. With traditional publishers turning their attention increasingly to mobile, and most Japanese firms still unproven in the broader international market, the question of what growth remains to this sector is a tough one - and its answer will determine whether the world's top mobile game companies soar or plummet in 2016.