Stock Ticker: Apple

Record results, but a huge drop in value. Why doesn't Wall Street love the other Big Apple?

Last night, after the closing bell on Wall Street, Apple announced its results for the quarter ended December 29th. The company - unarguably the most commercially successful technology company of the past decade, whatever your personal stance on its products may be - announced record revenue and profits, record sales of iPhones and record sales of iPads. Profits didn't grow vastly, remaining largely flat at just over $13 billion, but revenue shot up to $54.5 billion - $8 billion year on year growth, and a fairly stunning achievement for a company which only three years ago was boasting about making $50 billion a year. Now it manages that in 14 weeks.

Reaction on the markets was swift. Apple lost 10% of its value in after-hours trading.

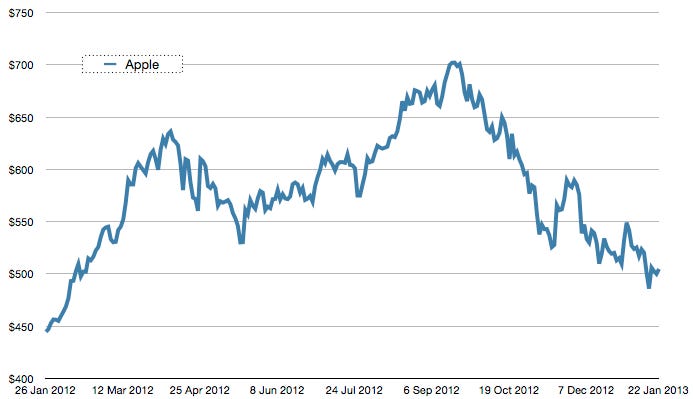

"Apple's share price has been sliding fairly consistently since it peaked at over $700 in mid-September"

Wait, what?

Yes, that's right - record figures for unit sales of the company's key categories (weak sales of Mac computers were a minor low spot, partially attributable to serious supply chain problems with the new iMac models which launched during the quarter), record turnover and record profits, all coming off the back of a year-ago quarter which was itself a remarkable record-breaker, drove Apple's share price down. In fact, Apple's share price has been sliding fairly consistently since it peaked at over $700 in mid-September, and this week it dipped below $500 for the first time since last February. You might reasonably have expected solid numbers to halt the decline; if anything, they accelerated it, at least temporarily.

So, what's going on here? Plenty of commentators have interpreted these figures as showing that Apple is hitting a wall in its growth. If you buy into the idea that the stock market reveals hidden wisdom in its movements, that's a fair assessment. A company which loses nearly 30% of its value in the space of a few months must have some underlying problem, or be facing some immense challenge which the market does not believe it can overcome. Right?

Well, maybe. The problem is that the stock market doesn't really move based on keen insight or solid fact - it is a beast driven more by sentiment and by the twin handmaidens of rumour and speculation. What Apple's precipitous drop means isn't that Apple necessarily faces its doom, it's that the market doesn't feel good about Apple - or worse, that it's not sure what to feel about Apple, since unpredictability is even worse than a fact-based negative outlook to a large extent.

"That's the kind of storyline investors can understand, and it's the kind of storyline that leads them to try to offload shares"

Recent months have seen a number of incidents which are, in the final analysis, of much more relevance to Apple's stock price (and the sentiment around the company) than they are to Apple's business. First, of course, there was the Apple Maps fiasco, which doesn't seem to have harmed iPhone 5 sales or iOS 6 installation rates, but reflected negatively on the company's image, at least in tech circles. Next, there was the negative response to the iPad Mini in the tech press, which was reflected in the financial press - although again, not in the consumer response to the device, which has been extremely popular. Finally, the past few weeks have seen whirling speculation about Apple missing some rather arbitrary financial targets in its results, fuelled in part by an unsourced, unverified but widely reported story about iPhone 5 component orders being halved.

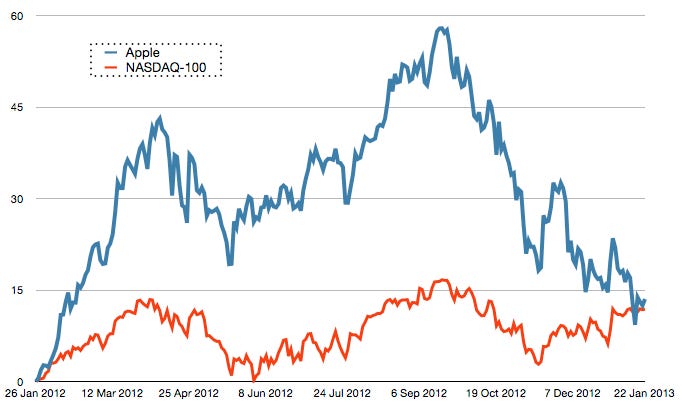

Add those things together, and you start to see a negative storyline forming around Apple - a company that's lost its shine, that's releasing products that aren't up to the quality or innovation of its former glories, and which is finally being punished with slack demand for its flagship iPhone 5. That's the kind of storyline investors can understand, and it's the kind of storyline that leads them to try to offload shares. Many of them bought Apple at well below $500 and will be happy to make money at that level, if they fear being exposed to significant risk by hanging on to Apple stock for too long. In a sense, they might even feel like what's happening now is just the hangover after the party - after all, recent years have brought Apple from stock market irrelevance to being among the world's biggest companies, vastly outperforming its market, the NASDAQ, until recent months dragged it back down to earth.

The problem, from the point of view of anyone who's actually trying to get a handle on where the tech market is going - a topic of some concern to anyone developing mobile and tablet games, to give a relevant example - is that the narrative the stock market has acted upon isn't really based on very many facts. As it does so often, the stock market is jumping at shadows. Look at Apple Maps and the iPad Mini - both derided in the tech press, both presented as examples of things "Steve would never have allowed" and added to the burgeoning narrative of a rudderless Apple failing to match up to the exacting standards of its late lamented founder and CEO, whose part in launching utter rubbish like MobileMe, iTunes Ping or the abortive iTunes Phone co-developed with Motorola is conveniently forgotten. Both of those products drove the share price down, yet it's clear that neither of them had a negative effect on actual revenue and profits, with the iPad Mini clearly driving holiday season revenue and Apple Maps more speculatively being attributed with helping the company to grow sales in China and other territories where Google's maps offering isn't very good. In other words, the markets got the one thing wrong they're expected to get right; they totally misread how a company's products would perform with consumers, preferring to be sucked in by the misgivings of the niche tech press.

"Who benefits from such a story being dropped into the press and circulated around the world? Well, in the world of stock trading, anyone who's got an option to sell Apple stock at over $500 in late January"

Of course, there's another question worth asking here, albeit a deeply cynical one. If the market is jumping at shadows, who's casting the shadows? That's a question worth asking with regard to Apple's other sentiment woes - especially the story about the reduced component orders for iPhone 5 handsets, which emerged, lacking any kind of source, in a small industry-watching publication before being picked up and vastly trumpeted in the financial press, including the Wall Street Journal (which should really, really have known better). Days later, there had been no confirmation and no more sources had come forward, and most publications quietly dropped the story about component orders being halved - but stuck to the narrative it had generated, namely that iPhone 5 demand is weak, even in the face of US carrier Verizon coming out with some solid, validated figures proving quite the opposite.

Follow the money. Who benefits from such a story being dropped into the press and circulated around the world? Well, in the world of stock trading, anyone who's got an option to sell Apple stock at over $500 in late January - which turns out to be quite a lot of people, with market commentators noting that the sheer volume of such options on the market suggests that quite a number of large investors and institutional traders had a direct interest in making sure that AAPL stock went below $500 around now. Stock manipulation, of course, is of dubious legality, but with the markets already nervous about Apple's meteoric rise and the abundance of "it hasn't been the same since Steve died" opinion pieces influencing the narrative, dropping some minor bombshells regarding the iPhone supply chain (truthful or otherwise) into the right ears would have been a huge temptation for traders sitting on such options. The lower Apple goes by the date their options come up, the more money they make.

This is the problem, in many regards, with a stock like Apple. The company is simply so huge that it's stock movements have become disconnected from its operations, and hooked up instead to a complex network of high-stakes gambles, bluffs and double-bluffs. Consider this; the 10% drop in Apple's share price after hours last night wiped enough money from its valuation to buy almost every one of its rivals in the mobile phone business, Samsung aside, twice over. Many people lost money when those shares moved, but many people made money, too. It's tough to believe that many of those people, with such sums at stake, would have been entirely passive in their involvement.

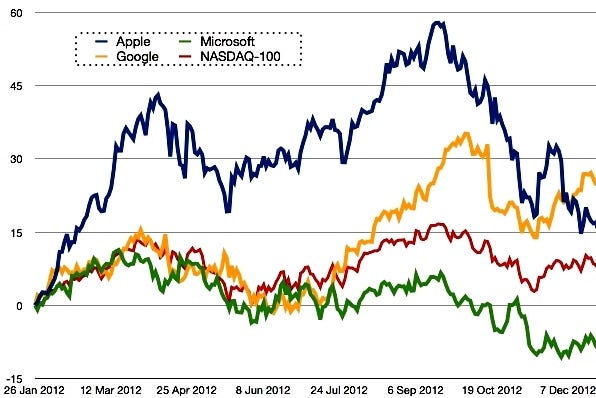

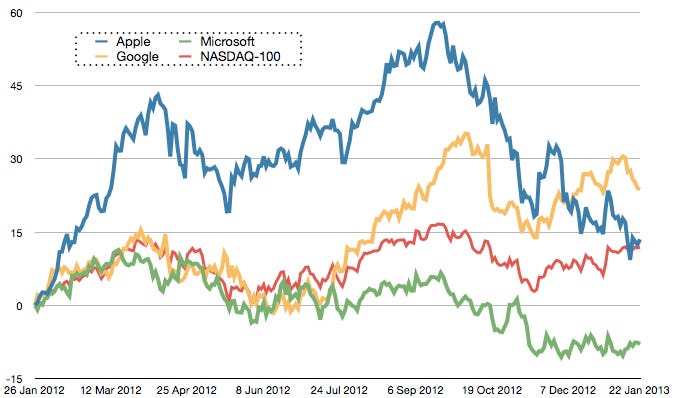

In a sense, then, Apple's sheer size compared to its rivals makes this next graph irrelevant, but it does still give us some idea of how the markets are thinking.

It should come as no surprise that despite the downturn over the past few months, Apple is actually vastly outperforming both of its closest US rivals, Microsoft and Google, over the long term. Google, however, is clearly seen to be backing a winner in the Android operating system - even if the only company that actually seems to be making serious headway from it in the mobile market is Samsung, whose share price we can't show here (we don't have access to Korean exchange data from our provider, so we can't plug it into our spreadsheets), but which has grown by a comfortable 45% over the same 12 month period, and would therefore be the top performer on this graph. Microsoft, however, is a tougher sell to investors. The response to Windows 8 has been muted at best, Windows Phone 8 is beloved of a small band of devotees and utterly unknown to almost everyone else, and few outside the same devoted band would argue that the firm's Surface tablets present even the remotest challenge to the iPad's dominance of the tablet market.

The reason this graph can't be taken at face value, though, is because of the sheer difference in the numbers it represents. In terms of overall value (market capitalisation), Google and Microsoft added together just about sum up to Apple's value. In terms of revenue, there's no contest - Apple turned over more money last quarter than Google makes in an entire year, and its annual revenue is more than double that of Microsoft. As for profit, again, it comfortably doubles Microsoft's take, and Google isn't even in the same ball park - Apple made more than four times Google's net income last quarter.

"In terms of overall value, Google and Microsoft added together just about sum up to Apple's value"

So what's the take-away for companies or individuals developing games for mobile and tablet platforms, and trying to figure out if there's anything to the claims that Apple has "disappointed" or worse, "hit a wall"? Simply this - Apple's fundamentals are incredibly sound, the company's sales are still growing solidly, and there are 75 million more iOS devices in people's hands now than there were three months ago. That's a lot of new potential customers. For investors, though, caveat emptor. Apple will probably grow again, simply because there's no evidence that the company's product growth is slowing or has been compromised, but it's going to take a while for the negative sentiment around the firm to dissipate - and as is inevitable with a stock this valuable in a market as volatile as technology, there are some very big sharks circling this gambling table.

Finally, I couldn't resist running this last set of numbers, even though the resulting graph made me a little sad. Steve Jobs was a die-hard devotee of Sony, and his dream through the early years of Apple was to model his company on the Japanese giant, whose product design, quality, work practices and market leadership he admired hugely. Today, even the recent downturn in the value of the Yen, which has bought Japanese exporters some breathing room, can't disguise Sony's continuing market decline - a decline for which Apple itself is heavily responsible. Apple's graph can be dismissed in part as a reflection of sentiment rather than reality. Sony's cannot.