DFC: Will Sony, Microsoft remain relevant in games by 2019?

Research firm sees PC and mobile grabbing larger and larger share of the expected $100 billion pie

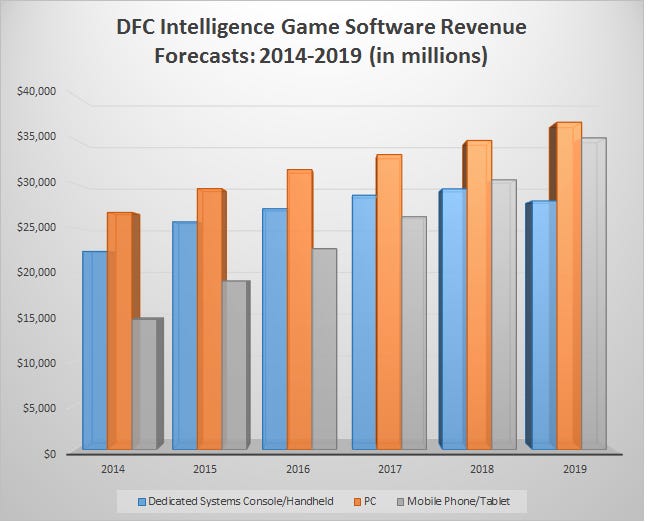

DFC Intelligence is once again preparing to release its latest forecasts covering the global games industry, and while the research firm is reiterating its $100 billion software revenues mark for year 2019, how the totals ultimately reach that mark may be slightly different than DFC previously estimated.

In a sneak peak provided to GamesIndustry.biz, DFC revealed that console forecasts are being lowered for Xbox One overall and for PlayStation 4 in North America. And while total console sales are expected to rise in China (not surprising given that the ban there was lifted), it's becoming clear that more and more of the revenue pie is coming from the booming mobile and PC segments.

DFC analyst David Cole expressed some concern about just how much relevance Sony and Microsoft will retain in the changing games landscape.

"This is the first generation of systems that really requires tech support and are in many ways behind what Steam has done for PC games and Apple has done for mobile devices"

"We have slightly lowered our forecasts for the Xbox One and Wii U. We see the PlayStation 4 remaining as the best-selling system with North America really being the only competitive market. Previously we thought the Xbox One could potentially outsell the Xbox 360 but now we don't think that will be the case. The real issue is by 2019 whether Sony and Microsoft will still be relevant in the game space. That is a major question mark," he noted.

"They really set unrealistic expectations for their systems and the issue is even as the gamer market grows they are really not growing their base in proportion. The PlayStation 2 was the best-selling console system ever and we don't see the PlayStation 4 beating it, even as the market has grown substantially. In other words, instead of expanding the market they have focused on a core base of users that could be ripe for the picking."

Cole added that aside from doubling down on the core audience, consoles may just be too complicated nowadays - an ironic step backwards from the days of the NES.

"We think the biggest issue is that the current generation of consoles have taken a step back in terms of usability. The beauty of game systems in the past was anyone could plug the systems in and be playing a game in seconds. This is the first generation of systems that really requires tech support and are in many ways behind what Steam has done for PC games and Apple has done for mobile devices," Cole said. "My kids have no problem playing their PC or mobile games but if I am out of town they have trouble getting on to the console systems. That is a BIG issue."

Cole believes that with the rise of other microconsoles that can play high-end games, Sony and Microsoft may no longer have a specific advantage.

"The competition to deliver high-end games to the television set is going to become intense and it is unclear whether Sony and Microsoft are prepared to compete in that space," he said. "You look at something like the Nvidia Shield and realize that is just one of a whole category of potential products that can go after this space. Right now Sony and Microsoft have the benefit of being the only platforms that can play high-end games on a TV but that will be changing."

He continued, "There are also the unrealistic expectations both companies set for their investors. Prior to the new generation launch there was speculation among some manufacturers and analysts that the market for this new generation could be as large as one billion units worldwide. We always thought success would be 250 million units combined for a given generation but now we don't see this generation doing that many. The PlayStation 4 could get over 100 million but the Xbox One will probably not reach that level. So clearly expectations were not set in line with reality."

DFC is forecasting that the market will be about 85 percent digital by 2019, and this will be largely driven by the growth in the PC and mobile space. Retail will still have a presence on consoles, particularly in North America and Europe, but digital is very quickly taking over.

Cole still sees Steam as the dominant force on PCs but there are plenty of revenue sources on PC that are helping to accelerate growth. "PC gaming is almost all digital and really it comes from many different places. Steam is dominant in what we think of as the traditional PC games sold on discs all over the place 15 years ago. Steam really just made the download experience somewhat seamless. Electronic Arts has made great strides with its Origin service but really we don't see anything on the horizon looking to give Steam a major challenge," Cole remarked.

"However, beyond Steam there is an entire diverse community of PC game products. Of course, Asia has its own infrastructure and Tencent is the largest game company in the PC game space. There are entire sub-segments of PC games that build audiences organically...not only the big names such as Minecraft, League of Legends or World of Tanks, but products like Animal Jam that target a whole new audience."

"When it comes to selling game software we think [VR] will be a rounding error in the near future"

While virtual reality is a big buzzword right now and the excitement around the technology was palpable during GDC this year, DFC remains unconvinced of its impact. "VR is likely to have a negligible impact on our forecasts. For one it is unclear whether games will be the primary application for VR. We do think VR has the potential to drive hardware sales and we will be releasing specific forecasts on that. However, when it comes to selling game software we think it will be a rounding error in the near future," Cole said.

As for mobile, DFC is raising its total forecast (in part due to even more expected growth in China) but the firm does see some headwinds with far too many games flooding the market. The category is regularly dominated by a handful of titles that far outperform everything else.

"The games business has always been about a few big products and everything else. The mobile space is not any different but the issue is compounded by lower barriers to entry," Cole said. "With console games it was about tracking hundreds of games. With PC it was thousands of games. On iOS alone in Q4 2014 we tracked nearly 100,000 game publishers (not just games). And of course, unlike with console and PC, it is really hard to get people to pay for games upfront. You have to give it away for free and the problem with 99.99 percent of games is the free version is all you need. It is a major problem for the industry as now you have AAA premium content and free content with very little middle ground. Our forecasts for mobile tend to be conservative because of that exact issue which we see will be hard to change."