Stock Ticker: Ubisoft

Rob Fahey puts Europe's last major publisher in the share price spotlight

Among the world's big games companies, Ubisoft is pretty much unique, for solely geographic reasons. It's the last of the major European publishing houses - the last man standing after a decade of attrition which saw the decline, acquisition or market exits of former rivals such as Infogrames, Eidos and Vivendi Universal.

Capitalised at over €600m (nearly US$800m) and with annual turnover of over €1bn ($1.35bn), Ubisoft is a major player in publishing. If it were listed in New York alongside its US rivals, Ubisoft's turnover would place it third - behind Activision and EA, but ahead of Take Two, and vastly ahead of any other rival in that market.

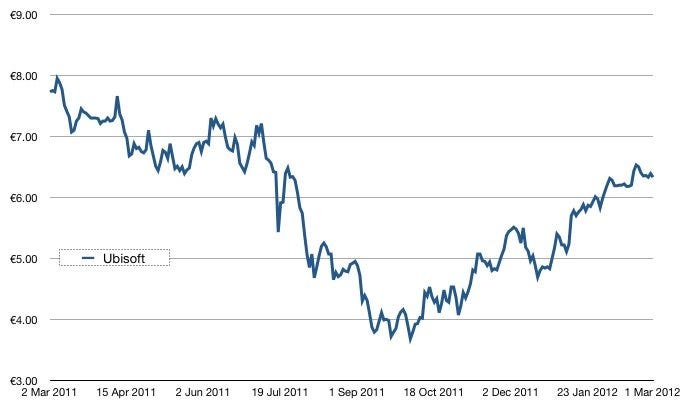

Yet if viewed from the perspective of market capitalisation, Ubisoft's valuation is only half that of Take Two - which is in itself suggestive of the difficulty of comparing a French company's stock performance against that of US rivals. Let's first view it in isolation, then - here's Ubisoft's performance on the Euronext Paris exchange over the past 12 months.

It's immediately apparent that Ubisoft didn't have a particularly stellar year - at its lowest ebb in September, the company's share price had lost half of the value it held at the beginning of this (slightly arbitrary) period. That said, the past five months have seen a pretty reasonable recovery. The firm's share prices have recovered much of their lost value, ending the year around 18% shy of their original valuation. Still, it's a long way from the firm's recent highs of over €16 in mid-2009.

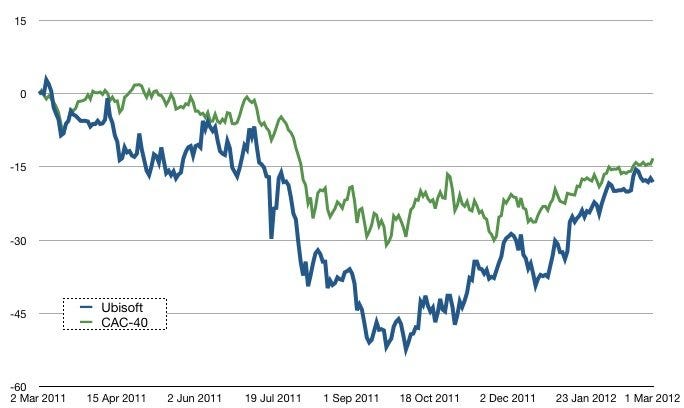

It's tempting to dive in and start looking for explanations for this graph's movements in Ubisoft's results and announcements over the past year, but as ever, it's helpful to first look at how the company's share price performance stacks up against that of its native stock market. For those purposes, I'm using the CAC-40, a commonly used index of the top 40 firms on Euronext Paris. Ubisoft isn't part of this index (although perhaps oddly, Activision Blizzard is, in a sense - Vivendi, one of the larger firms on the index, continues to own a controlling share in Activision Blizzard) but the CAC-40 is a reasonable measurement of the performance of shares in large French firms, and thus a good yardstick to use for Ubisoft stock.

As this graph shows fairly clearly, while Ubisoft has underperformed the CAC-40, it's not by any significant margin (it ends the period down 18% to the CAC40's 15%). The patterns look broadly the same - although it's troubling, at first glance, to note that Ubisoft shares did dip deeper and harder in late summer than the French index overall.

The company's fundamentals are much stronger than its share price would suggest - revenues are growing and the company should post a pretty healthy operating profit this year.

I'd argue that this is only natural, however. Europe is in the grip of a financial crisis which shows no sign of abating, and France's exposure to that crisis has been a matter of some debate for months. What you're seeing on this graph are largely crests and troughs based on rumoured changes to national credit ratings, speculation over the outcome of EU meetings in Brussels, or other major movements in market sentiment among understandably jittery investors. In such an environment, it's to be expected that Ubisoft - a smaller company trading in a volatile high-tech sector that few investors really understand - would get short shrift from nervous investors seeking safe havens, not risky gambles.

In short, I'm not sure how much we can read into Ubisoft's performance from its stock price. This is an important thing to bear in mind whenever we look at the markets - while it can be tempting to consider a company's graph in isolation and draw conclusions about the firm's performance from them, the reality is that a falling share price might not mean that investors have lost confidence in a specific firm at all. Rather, it might reflect an overall market trend; or, especially for high-tech stocks, it could reflect a nervous market fleeing into less high-stakes sectors, the financial equivalent of battening down their hatches.

In Ubisoft's case, the company's fundamentals are much stronger than its share price would suggest - revenues are growing, albeit slowly, and the company should post a pretty healthy operating profit this year. The fact that it's posting growth figures (it recently revised guidance for FY2011/12 up by around €10m, to between €1050m and €1080m) at a time when so many are questioning the future prospects of even major publishers is a very positive note.

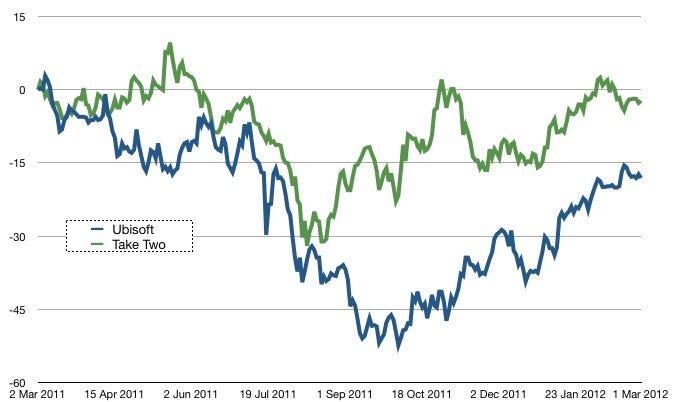

It's with this in mind that I think it's worth looking at a couple more comparative graphs - firstly, with Ubisoft's closest rival in terms of size, US publisher Take Two.

So, Take Two's stocks had a better year than Ubisoft's - that's undeniable. However, given the relative strengths of the markets in which these firms are listed, I'd say that these graphs actually indicate broadly similar sentiment among investors regarding these two companies.

That's about right, really. Take Two and Ubisoft occupy very similar market positions from a lot of perspectives. Neither of them is about to unseat EA or Activision from their top dog positions in the industry, but each of them has been very successful in boosting themselves out of the industry's "relegation zone" - the band of smaller to mid-range publishers who have been warned for years that unless they find a successful niche or build themselves up to a larger scale, they're going to crash and burn.

Should the French markets regain their confidence, an Ubisoft bounce seems inevitable.

For Ubisoft, the route out of that relegation zone has been through a genuinely impressive ability to create and exploit original IP. Over the course of the past decade, Ubisoft has created and perpetuated hugely successful franchises such as Splinter Cell, Prince of Persia (based on a previously dormant older IP), Just Dance and, perhaps most importantly, Assassin's Creed. Along with a stable of second-tier franchises which enjoy moderate sales (Tom Clancy licensed games (of which Splinter Cell is technically one), Far Cry, Brothers In Arms, Call of Juarez, The Settlers, etc.), this propels the company comfortably out of the danger zone and into the ranks of the big publishers. Take Two's strategy has been broadly similar, and once you allow for transatlantic differences, investors have reacted in broadly the same way.

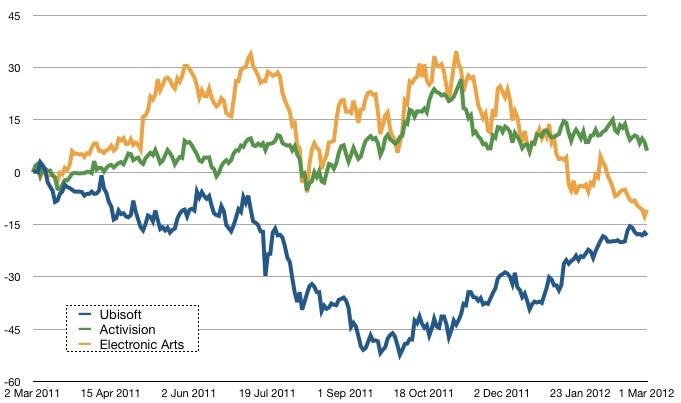

There are far fewer parallels to be found, however, in our last graph.

Here we see Ubisoft compared with the 800 pound gorillas at the top of the industry. At this stage, comparison is effectively impossible. Ubisoft trades in a different country and a very different economic climate to these two - and while Take Two's graph shows some points of comparison which suggest that some investors, at least, consider these two companies in a similar light, no such comparison points exist with EA and Activision Blizzard.

If we restrict our view to the past five months, though, a certain trend is evident. Activision's spike around the launch of Modern Warfare 3 aside, the firm's graph is fairly level, as it basically has been all year. Ubisoft has climbed slowly but surely since early Autumn. EA, though, is in a fairly sharp decline - investors remain nervous about the efficacy of John Riccitiello's approach at the company, and especially about the performance of Star Wars: The Old Republic, a title which I think many investors expected to be "EA's World of Warcraft".

What will be most interesting to watch, from a comparative point of view, is what happens to Ubisoft's valuation if the Euro crisis finds a satisfactory resolution in the coming months. For a company trading on a market where investors are worried sick about the safety of their money, Ubisoft has performed pretty well in the past year, and has managed to grow its business through one of the most challenging times imaginable for a European company. Should the French markets regain their confidence, an Ubi bounce seems inevitable - making it an attractive looking stock for those wishing to profit from Europe's presently depressed markets.